The Last Exit: Options for Fixing the Highway Trust Fund While Solvency is Still Solvable

Executive Summary

Congressional decisions on which transportation activities to prioritize and what funding levels to authorize are by no means easy decisions. But even more difficult is the decision on the source of funding for those transportation programs—so difficult, in fact, that there has been no decision made and no real funding solution provided for any of the transportation reauthorization laws passed since TEA-21 expired in 2003.

The source of revenues for these programs is critical because unlike programs that rely on annual appropriations, highway and transit programs are funded with contract authority from the Highway Trust Fund. Contract authority is a form of budget authority that confers many advantages; specifically, contract authority is considered mandatory spending, rather than discretionary, and therefore the cospending from the HTF does not need to compete with other spending accounts and priorities within the Transportation Housing and Urban Development (THUD) appropriation bill’s limits on discretionary spending (referred to as 302(b) suballocations). However contract authority is reserved for funding that originates from a trust fund with dedicated revenues. And without a decision for how to restore solvency, the trust fund has become steadily underfunded, such that it may become difficult to defend the use of that prioritized form of budget authority. No decision is also a form of decision, and before long the country may arrive at a point where eliminating contract authority or another onerous outcome is the only choice remaining.

Instead of continuing to slide toward that future, this paper seeks to lay out the options clearly to facilitate Congressional consideration and decision making. Fortunately, while the decision is difficult, the choices are fairly straightforward.

Congress can cut spending down to current revenues—although the path for that is already impossible for the transit account on its own, which could be cut to zero new spending and still require four years of current transit account revenues just to pay out the obligations from prior years. But by rebalancing the distribution between the highway and transit account, and cutting all new transit and highway authorizations by half, Congress could achieve Highway Trust Fund (HTF) solvency with no new revenue.

A second option: Congress can increase revenues to current spending. New revenues could take a variety of forms. Increasing the existing HTF revenues with an immediate 10 cent increase to the motor fuel taxes followed by gradual upward adjustments until they reach an increase of 17.8 cents per gallon by 2036 would close the solvency gap. New revenues could also be generated by vehicle registration fees or a VMT fee—a $120 registration fee on all vehicles would fill the shortfall by our calculations, and a VMT fee of 2.4 cents per mile fee would raise enough to replace all current revenues, although either option would involve addressing certain implementation challenges to ensure success.

Finally, there is the option to continue down the path of insolvency and for Congress to continue using the General Fund to support transportation programs, as has been done for the last 20 years now. Congress has steadily increased funding levels beyond revenues while also avoiding new taxes, and the de facto “solution” to enable this has been to backfill the shortfall with steadily larger transfers from the General Fund. This has taken the transportation programs to the point where in 2026, the receipts into the HTF will cover just 60 percent of its spending and that gap will continue to widen. In recent years, Congress has further expanded the amount of transportation spending outside of the HTF, in both annual appropriations laws and in a five-year advance appropriation in the Infrastructure Investment and Jobs Act (IIJA), which was designated as emergency spending.

It is possible that General Fund transfers and supplements will work for yet another cycle, and the highway and transit programs will continue to glide forward for another five- or six-year reauthorization period. However, an expiration date for that reauthorization would land in the mid-2030s, which will almost certainly ensure that discussions on HTF solvency become wrapped up in the insolvency crisis for the Social Security trust funds projected for 2032 and the Medicare Part A insolvency point in 2036. Amid this broader budgetary crisis it is dubious that transportation programs could continue to enjoy the advantages of contract authority spending when dedicated revenues cover just half of the actual spending. Determining a solution—before becoming embroiled in that wider set of revenue and spending challenges—will undoubtedly be to the benefit of those who prefer to see long-term funding that keeps pace with spending needs.

This paper explores how we have arrived at this point and seeks to objectively analyze each of the options for solvency: cut spending to meet revenues; increase revenues to meet spending; or keep using general revenue, either as bailouts to the HTF or as annual or advance appropriations. Any of these paths will bring substantial change to the HTF and the programs it funds, but it is just as clear that the current situation for the HTF is unsustainable. In the spirit of recognizing that change must come and analyzing all options, the paper concludes with a section on devolving the federal programs to states and evaluates state options for raising revenues instead.

Part 1: HTF Revenues, Spending, and Shortfall

I. The Past

In 1951, Congress declared it to be the policy of the federal government that federal services provided to any particular person or group should be paid for, to the extent possible, by fees or charges.[i] This principle, which is still on the books today, found an early expression in the Highway Revenue Act of 1956.[ii] This law increased taxes on highway users (mostly motor fuels excise taxes) to pay for construction of the new Interstate Highway System and other federal-aid road programs and created a new Highway Trust Fund (HTF) in which to hold the tax receipts until they could be spent.

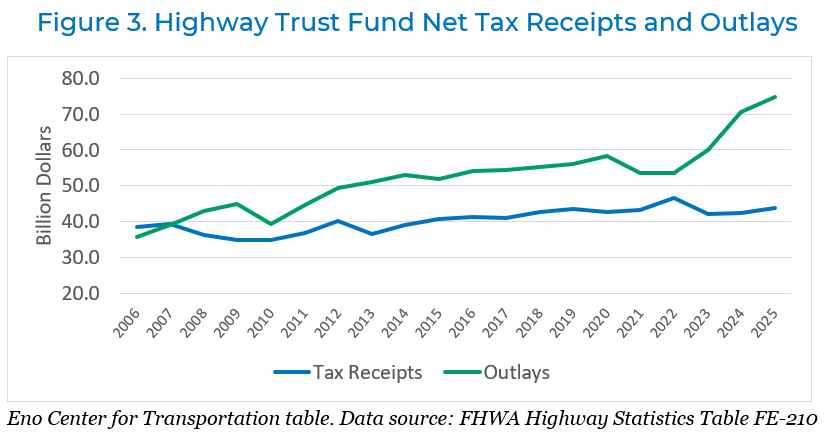

This construct worked well for its first 50 years, but since 2007, the system has become systemically insolvent, forcing Congress to provide $272 billion in bailout transfers from general revenues, the last of which is expected to run dry in 2028.

How did we get here, and how do we get out?

To begin with, we must recognize that the federal government has never been interested in how much motor fuel is owned by individuals or companies. Taxing motor fuel has always been a proxy for taxing the act of driving a motor vehicle on public roads, because it is far easier to tax a thing (especially when, as here, it is taxed at the point it leaves its place of manufacture) than it is to tax an activity taking place somewhere out in the world.

Unfortunately, basing federal road (and, later, mass transit) spending on the taxation of a proxy for driving has been subject to three long-term problems.

Problem #1: The amount of driving doesn’t grow like it used to.

In the “good old days” of the 1950s and 1960s, the amount of driving on U.S. roads, measured in vehicle miles traveled (VMT), increased at an average of 4.5 percent per year, a rate higher than inflation for much of that period. After the Organization of Petroleum Exporting Countries (OPEC) oil boycott and the Iranian revolution, the average rate of increase declined to an average 2.5 percent per year from 1979 t0 2002. Then, between 2003 and 2004, the price of gasoline made a permanent quantum jump from an average of about $1.20 per gallon over the 1991 to 2002 period to an average of $2.75 per gallon over the 2003 to 2014 period.

During the same period, widespread adoption of GPS-based navigation software in vehicles, especially in smartphones, made it easier for people to drive more precisely and efficiently between the same origin and destination points.[iii] Since then, VMT has only grown at an average of 0.8 percent per year, significantly below inflation.

The growth in VMT, and resulting growth in fuel consumption, meant that revenues to the HTF grew steadily, largely without lawmakers having to increase tax rates to account for inflation. The fuel tax rate was set at three cents per gallon in 1956; Congress increased that rate at several points such that it is now nominally six times higher than it was in 1956, but over the same 70 years inflation has increased by a factor of 12.

Taxing motor fuel is a proxy for taxing the act of driving a motor vehicle on public roads, but it has long-term problems.

Obviously, there was a significant disruption due to VMT during the COVID-19 pandemic. However, post-COVID, the trend has returned to its immediate pre-COVID level, with estimated 2025 VMT only 0.9 percent above the 2024 level. Current projections by the Federal Highway Administration foresee average VMT growth over the next 30 years to be around 0.6 percent per year.[iv] This is significantly below the Federal Reserve’s target inflation rate.

Problem #2: Motor fuel taxes are a worsening proxy for the amount of driving. In the mid-1960s, the average passenger car burned seven gallons of fuel to travel 100 miles. Today, that amount is down to around four gallons per 100 miles.[1] That 40 percent increase in fuel efficiency means that the tax is 40 percent less accurate as a proxy for the amount of driving taking place. The range of fuel economy has also grown wider as some consumers opt for larger or older vehicles, and others drive more efficient or non-gasoline fueled vehicles, which has further undermined the ability for gas taxes to serve as a user fee.

The rate at which this trend accelerates in the future is dependent on consumer demand for hybrids and electric vehicles, together with government policy to encourage purchase of such vehicles or to regulate fuel economy. But it is difficult to imagine that motor fuel consumption will ever become as accurate a proxy for the amount of driving as it once was.

Problem #3: Congress and the President have been unable to constrain spending to the level of tax receipts or to increase user tax rates.

Starting with the TEA-21 reauthorization bill, Congress began providing new spending authority that increasingly exceeded actual HTF financial resources.

Because these programs spend slowly, it took time for outlays—cash paid to reimburse non-federal partners for completed work—to catch up, but the cash-flow trend lines eventually followed suit.

[1] When comparing revenues raised based on a fixed per-gallon tax rate, it is helpful to invert the familiar miles-per-gallon ratio and look at gallons consumed per mile driven.

[i] U.S. Government Publishing Office. (1951). Public Law statutes at large: Vol. 65, p. 268–290. https://www.govinfo.gov/content/pkg/STATUTE-65/pdf/STATUTE-65-Pg268.pdf

[ii] U.S. Code. (n.d.). 31 U.S.C. § 9701—Fees and charges for government services and things of value. https://www.law.cornell.edu/uscode/text/31/9701

[iii] U.S. Department of Energy. (n.d.). Annual vehicle miles traveled in the United States. Alternative Fuels Data Center. https://afdc.energy.gov/data/10315

[iv] Federal Highway Administration. (2025, September). FHWA forecasts of vehicle miles traveled (VMT). U.S. Department of Transportation. https://www.fhwa.dot.gov/policyinformation/tables/vmt/vmt_forecast_sum.cfm

II. The Present

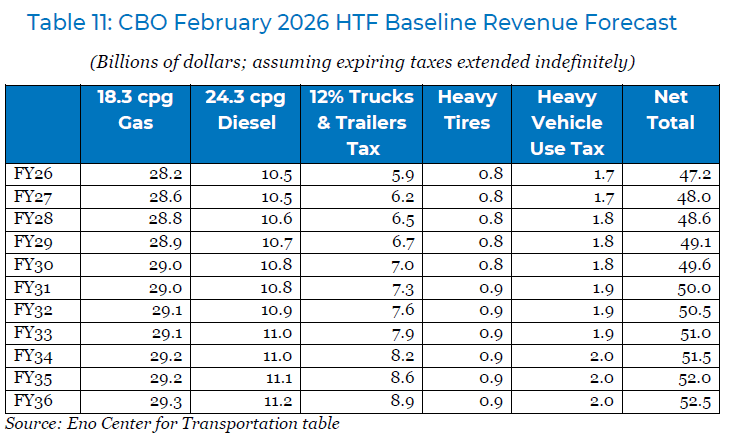

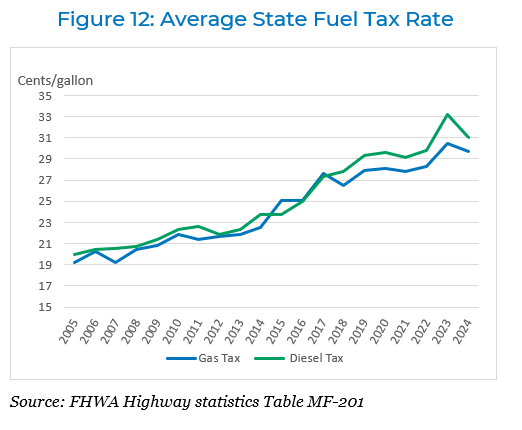

At present, the Highway Trust Fund is supported by five user taxes, the rates for which have not been increased since 1993 or earlier.

- An 18.3 cent per gallon tax on highway use of gasoline and gasohol.[1]

- A 24.3 cent per gallon tax on highway use of diesel and special fuels.

- A 12 percent sales tax on new tractors and trucks over 33,000 pounds gross vehicle weight (GVW) and on new trailers over 26,000 pounds GVW.

- A weight-based tax on tires with a load capacity over 3,500 pounds.

- An annual “sticker tax” on the use of heavy trucks over 55,000 pounds GVW, ranging from $100 to $550 per year.

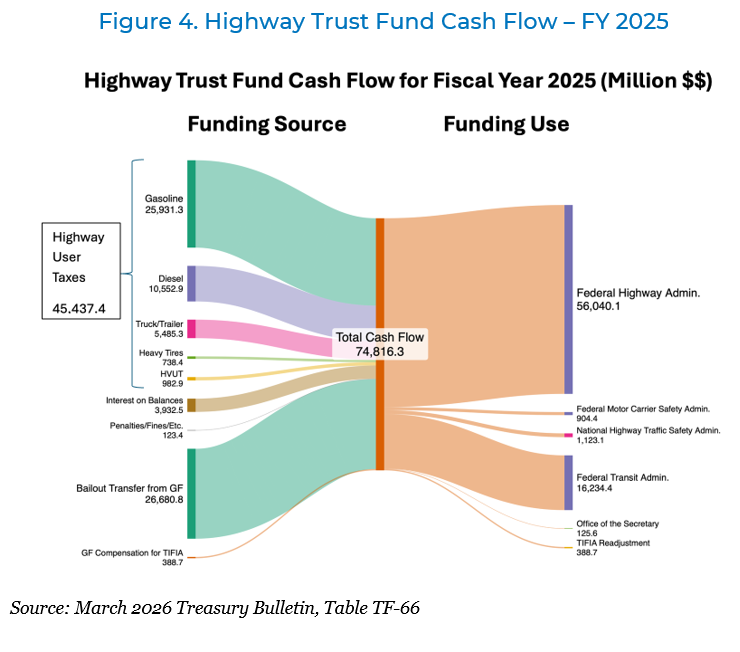

Figure 4 shows the relationship between actual tax receipts for these five user taxes with the rest of HTF cash flow in fiscal year 2025. The Trust Fund ended fiscal 2025 with $74.3 billion in positive balances remaining from the $118 billion bailout transfer provided by the Infrastructure Investment and Jobs Act (IIJA) in 2021.

[1] An additional 0.1 cent per gallon of gasoline and diesel taxes does not go to the Highway Trust Fund, instead being deposited in the Leaking Underground Storage Tank Trust Fund at the EPA to help clean up abandoned service stations.

III. The Future

The two official budget forecasting bodies (the White House’s Office of Management and Budget (OMB) and the Congressional Budget Office (CBO)) project future HTF spending and revenues based on a wide variety of factors and assumptions, including the VMT and fuel economy trends listed above.

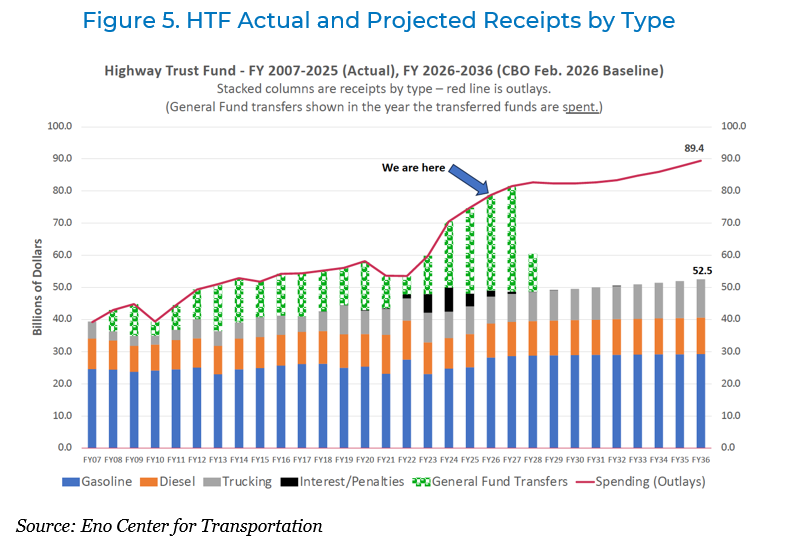

The law requires that the OMB and CBO’s “baseline” projections for future spending assume the most recently enacted fiscal year’s funding level from Congress, extrapolated into future years with annual inflation increases. For 99 percent of HTF spending, these are assumed to be the “obligation limitation” levels contained in the annual appropriations acts. The forecasters then model spending cash flow from these amounts based on historical patterns. For taxes, OMB and CBO are required to assume current law tax rates will be extended indefinitely and use economic and demographic modeling to project tax receipts. Figure 5 shows HTF cash flow since 2007, through the present, and into the future through the year 2036 via the latest CBO baseline projections.

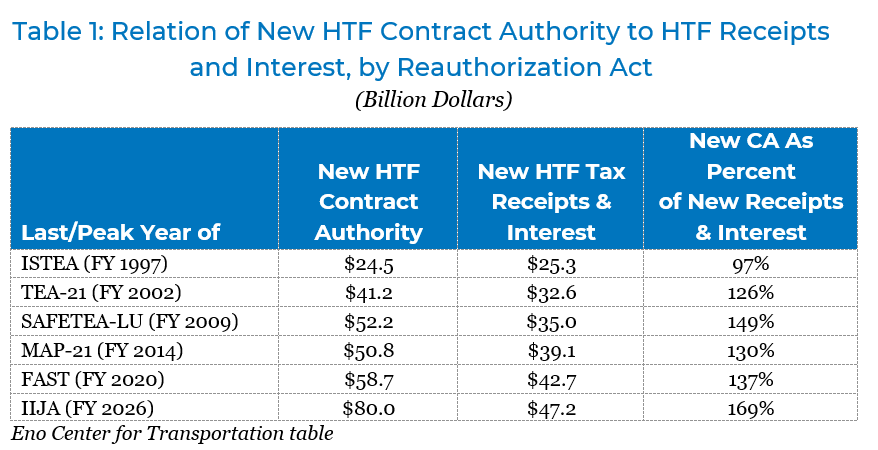

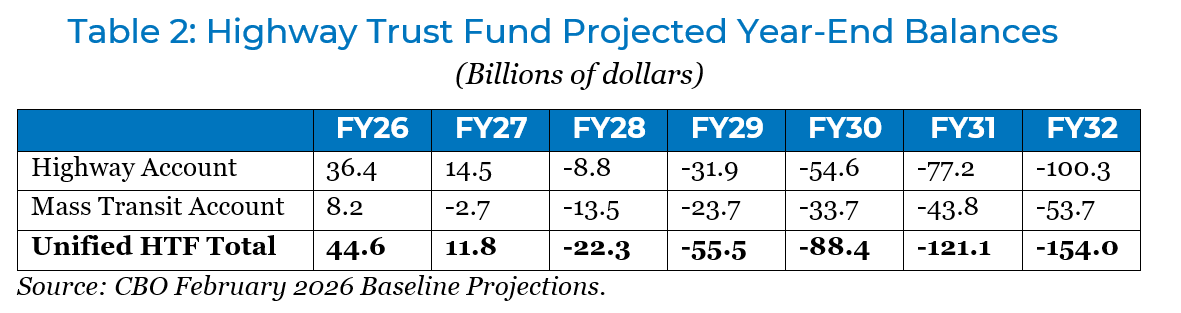

More specifically, Table 2 below shows the latest estimated amounts needed to avert Trust Fund insolvency in the short term. Assuming spending levels and tax receipts are consistent with the baseline, the Mass Transit Account will need almost $3 billion to complete a one-year extension of the IIJA. A two-year extension would see the Highway Account go insolvent as well, with a total of $22 billion in either outlay reductions or additional deposits needed to keep both accounts solvent through September 2028.[1]

A five-year reauthorization is the minimum length sought by state transportation departments, who need to know approximate levels of future federal funding support in order to plan project development. This would require $126 billion in additional deposits in order to maintain current spending levels (plus inflation) including cash cushion. For a six-year bill, which was the standard length of the 1991 and 1998 reauthorization laws, that total rises to $159 billion in additional deposits.

As Congressional negotiators consider the next reauthorization of the surface transportation programs, the source of funding for those programs and the solvency of the Highway Trust Fund are central issues to be resolved. This paper explores the solution set for those questions. Put bluntly, the options are simple—Congress can choose to close the revenue gap:

- On the outgo side by shrinking the Trust Fund spending levels,

- On the income side by increasing dedicated Trust Fund revenues,

- Through some mix of (a) and (b); or

- They can continue to allow the Trust Fund shortfall to grow through the transfer of additional General Fund revenues.

In addition to the question on revenues, Congress will also need to decide whether to continue the elevated levels of spending provided in IIJA through Division J, and if so, whether to include those programs in the HTF. That issue is explored in Part 2.

[1] In addition to the amount needed to get to an end-of-FY zero balance, a “cash cushion” of extra money is needed to ensure that program agencies don’t run out of cash on a day-to-day basis while waiting for twice-monthly tax deposits. Congress has been assuming a $4 billion cushion for the Highway Account and a $1 billion cushion for the Mass Transit Account as the appropriate levels.

Part 2: IIJA Advance Appropriations: One Time Emergency or a New Normal for Funding?

Despite the IIJA increases in HTF spending that well exceeded receipts, as Senate negotiators were crafting the 2021 bipartisan infrastructure law, they were unable to increase total HTF contract authority to levels adequate to fund all of the surface transportation programs envisioned by the bipartisan compromise, even with a $118 bailout transfer of the HTF by the General Fund. Accordingly, Division J of the IIJA also provided an unprecedented $446 billion in “advance appropriations” from the General Fund for guaranteed support of select infrastructure improvements.

What was in the IIJA’s Division J

Of that amount, $184 billion was for the Department of Transportation. After removing aviation, maritime, and pipeline programs, almost $156 billion of these advance appropriations went to surface transportation modes and grant programs over five years. That included an unprecedented $71 billion in “advance appropriations” from the General Fund beyond the IIJA’s $383 billion in total HTF contract authority for the four modal administrations normally dependent upon the HTF, resulting in a guaranteed program total of $454 billion over five years. It also included $66 billion for the Federal Railroad Administration, as well as $19 billion for four grant programs administered by the Office of the Secretary: National Infrastructure Investments (variously known as TIGER, RAISE, or BUILD); Safe Streets and Roads for All; Culvert Removal grants; and the Strengthening Mobility and Revolutionizing Transportation grant program.

As a result, IIJA led to a mix of funding sources for each mode. The relative dependency of each modal administration on the HTF versus General Fund advance appropriations and annual appropriations is shown in the table below.

This paper focuses on the HTF and how to address the future costs—at “baseline levels”—for the budget accounts, programs, and activities currently supported by the HTF. However, another major question that Congress will face for the next reauthorization is whether to grow the programs beyond the HTF baseline and specifically whether to continue funding levels at the IIJA level or beyond. While the $156 billion in advance appropriations from IIJA for surface transportation programs at USDOT are not considered part of the HTF “baseline”, many Congressional negotiators will have interest in continuing some of these programs.

Non-federal partners have also come to rely on some of this money, particularly the $6.75 billion per year of the FHWA funding and the $1.0 billion per year of the FTA funding that is distributed widely to state and local governments via formula. As a result, maintaining the HTF funded accounts at baseline levels and discontinuing the advance appropriation-supported programs may be experienced as a cut to spending.

Extending Division J in the Trust Fund

This section estimates the cost of extending the Division J programs at baseline level, either through the HTF structure or through some other means other than regular, annual appropriations.

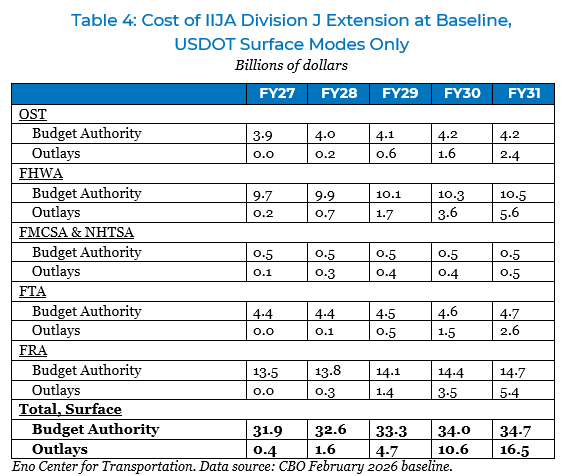

Since the IIJA was the first surface transportation law to include an appropriation of funding for intercity rail; on the one hand the lack of any other source of guaranteed funding may make the intercity rail funding a higher priority but on the other hand the inclusion of rail was somewhat controversial and there are calls to return to a “traditional” funding approach. Therefore, we are presenting two lines of analysis: one that extends IIJA Division J funding for all surface transportation modes except the Federal Railroad Administration (FRA), and one that includes FRA as well.

To begin with, we must reiterate that infrastructure capital programs spend very, very slowly, and many of the IIJA Division J programs are among the slowest of them all. In the case of these programs, this slowness, combined with a budget technicality, may present policymakers with choices that look easier than they actually are.

The cash outlays from the five years of advance appropriations provided by the IIJA (FY 2022-2026) are already built into the baseline for future spending and will occur whether or not Congress extends the programs past their expiration in 2026. In other words, the ongoing outlays from the funds appropriated under IIJA will not count against the next reauthorization law.[1] If Congress chooses to continue to fund these programs starting in FY 2027 and beyond—whether out of the HTF or as advance appropriation or some other kind of guaranteed multi-year funding—only the new outlays derived from new budget authority provided in 2027 and future years would be scored against the new legislation.

In order to maintain IIJA funding levels, Congress could provide $156 billion in additional funding for surface transportation. Eventually the Treasury would have to start paying significant amounts of money to liquidate these new spending commitments, but due to the combined effect of slow spending rates and this “reset” of the outlay flow, there would be a delay of several years before costs became significant.

A five-year extension of all the Division J surface transportation appropriations, including rail, at baseline levels would provide an additional $166.5 billion in new spending commitments, and over the ten-year budget forecast window outlays would eventually catch up to those new promises. By 2036, the baseline of new budget authority would be $38.2 billion and outlays will have risen to around $33 billion per year. But critically, only $34 billion in spending would come due by the end of a five-year reauthorization bill. In other words, if Congress made the funding available but only paid for the outlays to occur during the 5-year bill itself, they’d be leaving 80 percent of the cost of that spending for a future Congress to address.

Increasing spending levels while only covering the costs of immediate outlays leaves an ever larger shortfall for future laws to address –this is essentially how we’ve gotten to such an unsustainable place for the Highway Trust Fund.

This construct of increasing spending levels but only ensuring funding suffices to cover the immediate outlays while leaving an ever-larger cost for future laws to cover is essentially how we’ve gotten to such an unsustainable place for the Highway Trust Fund. For Congress to fund Division J programs for five more years while only concerning itself with paying for the outlays that come due during that initial spending reset period would extend this highly irresponsible approach and would make federal support for transportation infrastructure programs even less reliable in the long-term.

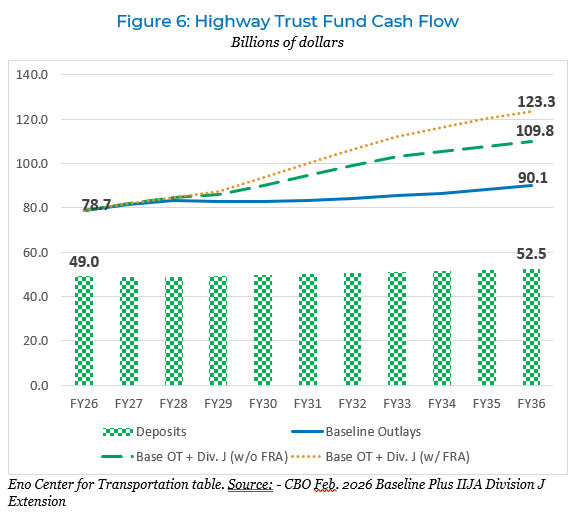

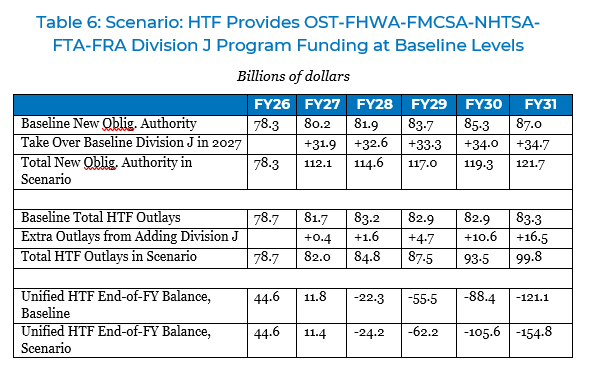

The following chart shows the latest baseline projections for Trust Fund receipts and interest (green columns) and outlays (blue solid line), with the difference between the two totals rising modestly from $30 billion per year in 2026 to $38 billion per year in 2036. If you add all of the IIJA Division J programs at baseline levels (including the Office of the Secretary’s grant programs, but excluding FRA), you get the dashed orange line, and the difference between baseline revenues and outlays rises to $57 billion per year in 2036. If you add Division J FRA spending on top of that, the gap between baseline revenues and spending rises to $71 billion per year in 2036.

Highway Trust Fund takes on Division J – excluding FRA

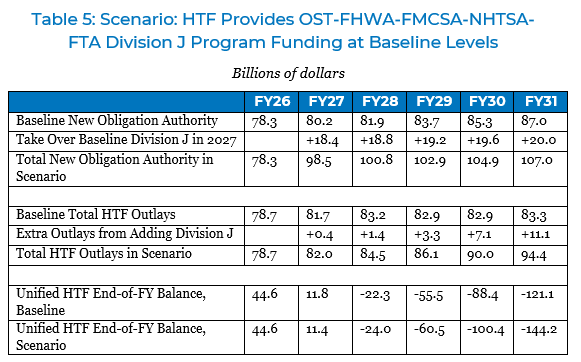

If Congress were to fund IIJA Division J accounts for OST, FHWA, FMCSA, NHTSA, and FTA for five years at baseline levels out of the HTF, this would add $96 billion in new budget authority. Additional outlays of $23.1 billion would need to be covered to maintain solvency over the five-year period. Combined with the existing HTF revenue gap, the amount of extra HTF deposits needed to fund a five-year bill at baseline would be around $149 billion ($144 billion plus a $5 billion minimum prudent cash cushion).

Table 5 explores this scenario of the HTF being expanded to provide funding for all the surface transportation programs from IIJA Division J with the exception of FRA funding.

Highway Trust Fund takes on Division J – Including FRA

If Congress were to fund the above Division J programs from the Trust Fund and then also add Federal Railroad Administration Division J programs at baseline levels, total additional budget authority would be $167 billion over five years but outlays over the first five years would only be an additional $34 billion because of the unbelievably slow outlay rate of the large rail programs.

The additional amount needed to keep the Trust Fund solvent at baseline would rise to $160 billion ($155 billion to zero plus the $5 billion cash cushion).

Once more, we emphasize that the downstream effects over the following five years (2032-2036) require significantly more federal funding. See the ten-year tabular appendix for details.

[1] The outlays from the 2022-2026 budget authority will still be charged to the Appropriations Committees’ regular allocation with an off-budget emergency designation.

Part 3: Maintain Current Spending Levels Without Increasing Trust Fund Tax Revenues

If Congress decides to maintain current spending levels from the HTF without increasing excise tax revenues, then they will need to transfer money from General Fund. In this case, Congress will still need to answer two questions:

- Will the General Fund financial support be transferred into the HTF and provided as contract authority, or will it be provided outside, and in addition to, HTF dollars?

- Will Congress offset the cost to the Treasury of the General Fund financial support, in whole or in part, by cutting spending or increasing revenue elsewhere in the budget?

Question One: Where will General Fund support be transferred?

Option 1. Transfers into the Trust Fund

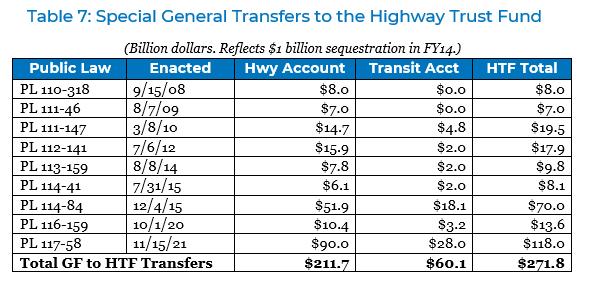

Transferring general revenue directly into the HTF is the “path of least resistance” that Congress has been pursuing since September 2008. On nine separate occasions, Congress has passed laws making new General Fund deposits into the HTF, totaling $271.8 billion.[1]

The operative language of a transfer is very simple—just one sentence, this one from the first such law (P.L. 110-318) in September 2008: “Out of money in the Treasury not otherwise appropriated, there is hereby appropriated to the Highway Trust Fund $8,017,000,000.”[2]

Per the CBO’s February 2026 baseline, if Congress were to pursue this approach and provide the full transfer up front to offset the estimated cost of a five-year reauthorization at current spending levels plus inflation, the required transfer would total $126 billion. That would bring cumulative General Fund support for the Highway Trust Fund from 2008 through 2031 to $398 billion.

The benefit of General Fund transfers into the HTF is primarily that it is a facile (if short-term) solution that does not require any changes to funding distribution nor run afoul of anti-tax pledges. Transferring money into the Trust Fund also enables those dollars to be provided as contract authority, a unique form of budget authority that is classified as mandatory and is exempt from various budget controls including sequestration.

For bailouts that enable programs to stay solvent at levels that have already been authorized, proponents of transfers emphasize that it is fundamentally unfair for the federal government to refuse to pay its debts by withholding reimbursement to states for authorized work already done and paid for out of state finances.[3] If Congress is unable to align Highway Trust Fund spending authority with projected Highway Trust Fund tax receipts, General Fund transfers ultimately become necessary to ensure payments of money obligated by the federal government to states and other non-federal partners.

And if the federal government withholds reimbursement for long enough, states can, and have, filed suit against the Department of Transportation in the U.S. Court of Federal Claims —and won. This results in the court ordering the reimbursement paid, either by USDOT from the Trust Fund or, if necessary, by the court itself from the “Permanent Judgement Appropriation” (31 U.S.C. § 1304), which is part of the General Fund. From this perspective, a General Fund bailout of the HTF in order to make reimbursement payments on time is more efficient than making states wait for a year or more to get reimbursement payments (plus interest) from the General Fund through the Court of Federal Claims.

Opponents of these transfers point out that the Highway Trust Fund was created and given privileged budgetary treatment under the “user-pay” principle, and that making general revenues fungible with special user taxes effectively nullifies the whole user-pay rationale underlying the HTF.

They also say there is nothing special about highway and mass transit programs in particular that should give them privilege above other transportation modes, not to mention all other programs in the federal budget, and allow them to print money as needed to pay their bills. Defense, education, law enforcement, housing, environment, and most other functions of the government face more built-in constraints on their spending levels than do Highway Trust Fund programs in the age of automatic General Fund bailouts.

Opponents also point out that, as long as spending continues increasing while excise tax rates remain unchanged, and tax receipts stay stagnant, every General Fund transfer simply delays the inevitable reconciliation of the HTF’s spending and revenue lines as they continue to spread farther apart. In other words, each General Fund transfer allows the HTF’s financial hole to deepen.

General Fund transfers have been relied upon to pass three transportation reauthorization laws and multiple extensions across nearly two decades, but as revenues and spending decouples, they may become an unsustainable option. In addition, regardless of what Congress does this time, the overall federal attitude towards simply bailing out trust fund accounts as necessary to prevent default may change by 2032, which is the estimated insolvency date of the Social Security Trust Fund. If the American people have to endure epic, once-in-a-generation budgetary pain to keep Social Security solvent in the early 2030s, there may be much less political support afterwards for continuing to bail out the Highway Trust Fund.

Option 2(a). Providing Funds Outside the Trust Fund – Regular Appropriations.

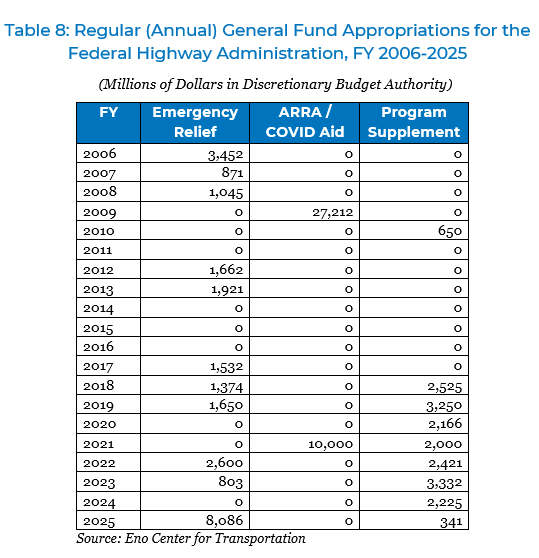

Congress has always had the option of making annual appropriations for transportation funding. For highways, over the last 20 years, Congress has intermittently used the annual appropriations bills to provide the Federal Highway Administration with total additional amounts of $25 billion for emergency relief highways, $37.2 billion for economic aid during recessions, and $18.9 billion to create or supplement highway programs that are of particular importance to Congress.

As table 8 shows, the delivery of this funding is somewhat lumpy, and the nature of the annual appropriations process makes it impossible for state and local partners to rely on anticipated funding in advance with any degree of certainty, which makes it difficult to plan large projects.

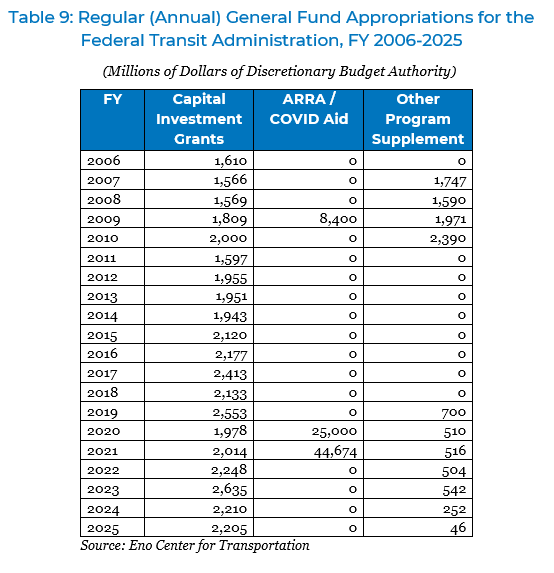

For mass transit, the picture is more complicated. For its first decade, the federal mass transit program was completely supported by the General Fund. Even after 1982 when the Mass Transit Account was established in the Trust Fund, those contract authority dollars were still less than half of total federal transit spending. Since the late 1990s, the HTF’s share has settled near 80 percent of total mass transit spending—a much lower share than highway programs. The remainder is provided from the General Fund in the annual appropriations bills, primarily for the Capital Investment Grants program.

General Fund support through the annual discretionary appropriations process can be difficult. Congress rarely passes the appropriations bills on time, necessitating short-term extensions and hampering planning. For 23 of the last 35 fiscal years, annual discretionary appropriations have been subject to some kind of sequestration-enforced spending cap, which forced all non-defense programs to fight against each other for scarce resources. And the word “discretionary” implies unpredictability—it means that Congress has the legal discretion to zero out funding for any program in any fiscal year without exposing the federal government to legal liability. That kind of certainty is the opposite of what is needed to build slow-spending capital projects.

Option 2(b). Providing Funds Outside the Trust Fund – Advance Appropriations.

The unpredictable nature of the annual appropriations process has meant that state and local transportation stakeholders demand much of their federal financial aid guaranteed several years in advance. On the highway side, there was formerly a bifurcated process from the end of World War II through the late 1970s, where the regular program was funded up to three years in advance and construction of the Interstate program was funded up to a dozen years in advance.[4] By the late 1970s, most of the Interstate had been completed, so the duration of the authorization laws grew to between four and six years—the “sweet spot” where state partners felt comfortable engaging in five-year capital construction plans dependent on forthcoming federal aid.

This goal of advance certainty for capital programming can be achieved outside of the HTF through advance appropriations, such as those used to supplement IIJA contract authority. Advance appropriations are enacted into law in a certain fiscal year and then become available for obligation in a later fiscal year without requiring additional Congressional action. The $71 billion in IIJA advance appropriations for USDOT were enacted in fiscal year 2022, and 20 percent became available for fiscal year 2022, 20 percent for fiscal year 2023, and onwards through fiscal year 2026.

Once enacted, General Fund advance appropriations are just like HTF contract authority in that a subsequent Act of Congress would be required to repeal the funding.

The passage of advance appropriations can also pose some difficulties. Advance appropriations were popular for federal construction programs in the 1960s and early 1970s but were also considered a form of “uncontrollable spending” (e.g., pending outlays that cannot be reduced by Congress by lowering the amounts provided in the annual appropriations bills). In the 1970s, the growth of “uncontrollable spending” led to a reform movement that culminated in 1974 in the creation of a Congressional budget process that still governs Congressional spending.[i] Since then, the Budget Committees have tried to discourage the growth of advance appropriations in the regular budget.

Accordingly, advance appropriations are either subject to the regular budget controls, including the regular budget ceilings that govern the Appropriations Committees and their bills, or they may be declared an unforeseen emergency, so that the spending does not count toward the budget ceilings. However, the Budget Act requires that each individual appropriation given such an emergency designation is subject to a 60-vote point of order in the Senate, whereas regular appropriations that are subject to normal budget ceilings only require a simple majority vote in the Senate. In 2021, Congress chose to use advance appropriations in the IIJA, designating the funding as emergency spending, and passed the final bill with more than 60 votes.

[1] Congress has also transferred $3.7 billion from Leaking Underground Storage Tank Trust Fund to HTF since 2007, but this support is consistent with the user-pay principle, since all those tax receipts were paid by highway users. Current balances in the LUST Trust Fund only total around $1.7 billion.

[2] There is always money in the Treasury (unless we are in the final handful of days of a debt ceiling crisis).

[3] Most Trust Fund grants are reimbursable grants – states or other non-federal partners actually perform work at their own expense, and once that work is completed, the non-federal partner then requests reimbursement from the Department of Transportation for a fixed share (at least 80 percent) of the amount spent. Reimbursements are often same-day or next-day.

[4] The 1956 authorization law provided contract authority for the regular highway program for fiscal years 1958 and 1959 and provided Interstate Construction contract authority for fiscal years 1958 through 1969, for example.

[i] Congressional Budget and Impoundment Control Act of 1974, Pub. L. No. 93–344, 88 Stat. 297 (1974).

Question Two: Will Cost to the General Fund be Offset?

The first few General Fund transfers to the Highway Trust Fund were not accompanied by any sort of budgetary offset (“pay-for,” in layman’s terms). As such, when the transfers were eventually used to pay bills and make outlays, every dollar of those outlays added to the federal deficit.

The transfers made from 2012 through 2015 were, for the most part, offset via some combinations of reductions in mandatory spending and increases in federal user fees, as measured over a ten-year budget enforcement window. This was due to the efforts of Rep. Paul Ryan (R-WI), who as chairman of the House Budget Committee from 2011-2015 and then as Speaker of the House starting in October 2015, used his position to insist that such transfers be offset.

Some of the “pay-fors” were of dubious merit, particularly the “pension smoothing” used to offset $8.7 billion of the $18 billion transfer in the 2012 MAP-21 law. (Pension smoothing reduces federal spending during the ten-year budget enforcement window but increases spending by a greater amount after the ten-year window expires.) But because those pay-fors qualified as offsets under the same budget rules that apply to all other programs, Ryan was able to claim that the Highway Trust Fund did not get special budgetary treatment under his watch.

None of the $118 billion General Fund transfer made by the 2021 IIJA infrastructure law was offset, and the old “Ryan rule” was not part of the Congressional budget resolution adopted by Republicans in 2025, so no offsets for General Fund transfers to the Highway Trust Fund are currently required under law or House or Senate rules.

Part 4: Closing the Trust Fund Gap by Reducing Federal Spending

The HTF could be made solvent again by cutting future spending but it would not be easy because so much of outlays in the next few years will be reimbursements of spending authorized in past years.

Highway Trust Fund Revenues and Spend Out Rates

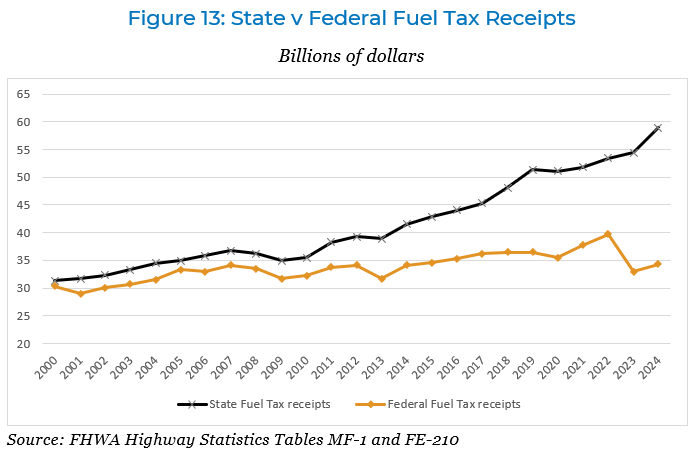

The Highway Trust Fund has access to significant dedicated tax revenues of around $50 billion per year. Some believe that this amount of taxation should be sufficient to support all highway and mass transit programs of truly federal concern.

If Congress were to decide to make the Highway Trust Fund solvent once more solely by reducing spending, a dizzying number of policy decisions would be required—which programs to protect, which programs to target for reduction or elimination, and how to deal with the various political and economic consequences of each program cut or killed.

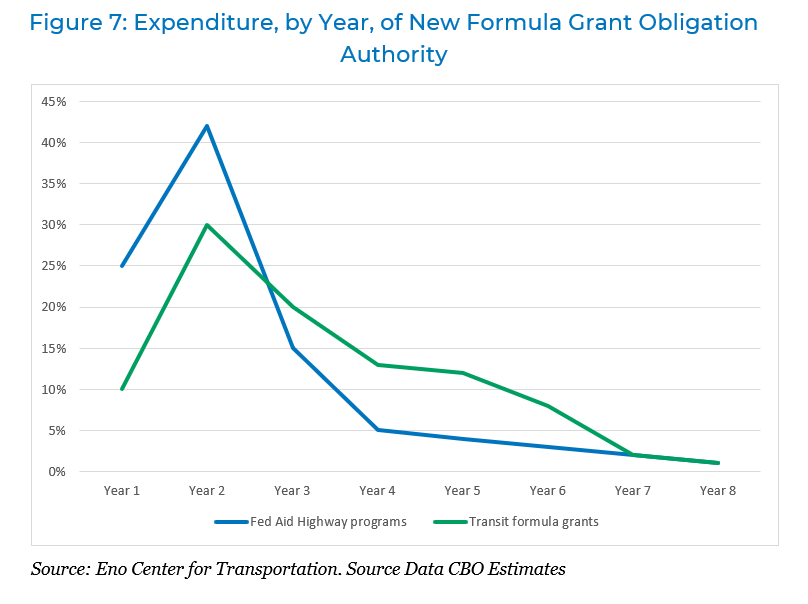

But all of those policy decisions are subject to one mathematical truism: Highway Trust Fund capital programs spend their money very, very, very slowly, and because of this, spending cuts ordered by Congress take years to be fully realized through reduced outlays.

Congress can only control the rate at which new contracts and other spending commitments are finalized, not the time which non-federal partners take to spend funds available through previously signed contracts. For every dollar in new contract authority and obligation limitation provided by Congress in legislation for a given fiscal year, CBO estimates how much of that dollar “spends out” via outlays in that first year and in every subsequent year.[1]

For example, by far the largest budget account funded by the Highway Trust Fund is Federal-Aid Highways, which constitutes the bulk of the Federal Highway Administration’s budget. CBO estimates that 25 cents of every new dollar of obligation authority leaves the Treasury as outlays in the first year that the new authority is available.

The 25 percent first-year outlay rate means that, if Congress wanted to reduce HTF outlays from the Federal-Aid Highways account by $5 billion in the upcoming year, they would have to reduce new contract authority and obligation limitations on the account by $20 billion in that first year.

The only mass transit budget account funded out of the HTF is now Transit Formula Grants, and it spends out even more slowly than does the highway program, with a 10 percent first-year outlay rate.

Highway Trust Fund capital programs spend their money very, very, very slowly, and because of this, spending cuts ordered by Congress take years to be fully realized through reduced outlays.

If Congress wanted to reduce HTF outlays from Transit Formula Grants by $5 billion in the upcoming year, they would have to reduce new contract authority and obligation limitations by $50 billion in that year, which is impossible, since new spending authority only adds up to around $15 billion per year. Any spending cuts to mass transit will take several years to be fully realized.

[1] When an agency obligates funding, they incur a legally binding commitment; the outlay occurs when the agency settles that obligation. While outlays can take many years, the agencies ensure that funding is obligated up to the authorized level for that year.

[i] Congressional Budget Office. (2026, February). The budget and economic outlook: 2026 to 2036. U.S. Congress. https://www.cbo.gov/publication/

Highway Account: Spending Cuts Needed for Solvency

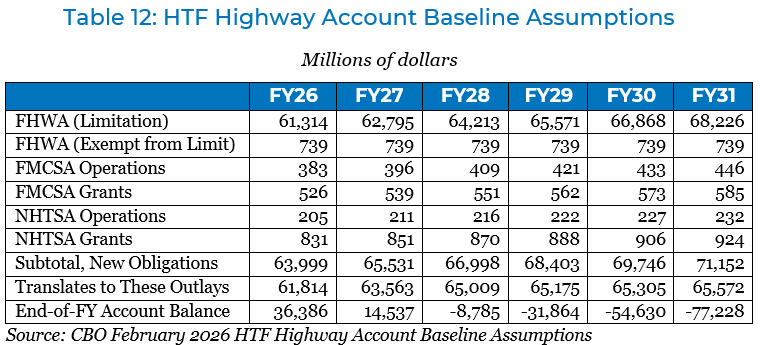

Below are the assumptions for new spending authority for the Highway Account of the Highway Trust Fund in the Congressional Budget Office’s February 2026 baseline forecast.[i] These are the levels in effect for fiscal year 2026 at the time the baseline assumptions were “locked” (January 14, 2026, when a continuing resolution at 2025 levels was in effect), plus annual inflation increases. The table also shows the estimated Account outlays and end-of-year balances.

For this exercise, we will leave the baseline assumptions for FMCSA and NHTSA accounts intact, because (a) the official message at USDOT, from the Secretary on down, is safety first, and (b) everything else in the Highway Account but the main FHWA account adds up to a rounding error by comparison.

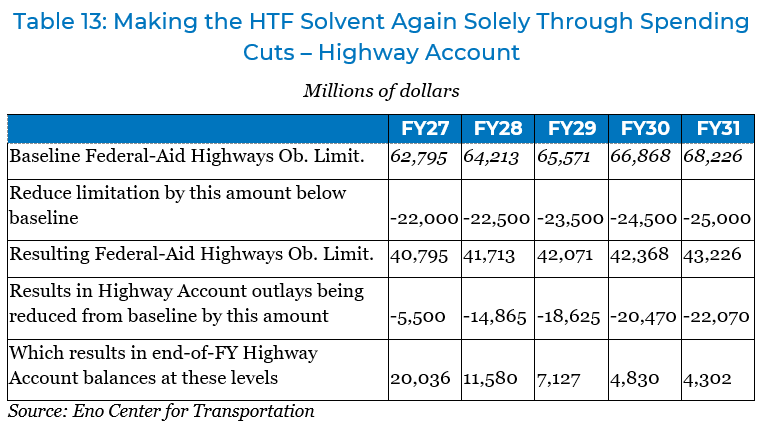

An immediate $22 billion spending reduction from baseline followed by increasing annual reductions up to $25 billion below baseline by 2031 would ensure Highway Account solvency

We ran various scenarios for reduction of the Federal-Aid Highways obligation limitation in half-billion-dollar increments, looking for the smallest reduction that would allow a five-year reauthorization bill that ended up with both an end-of-2031 Highway Account balance of at least the $4 billion cash cushion, and a relatively solvent trend line after 2031.

We found that an immediate $22 billion reduction from baseline, with continuing reductions on an annual basis until it reached a $25 billion reduction relative to baseline in 2031, was the minimum necessary to ensure Highway Account solvency solely by means of spending reductions.

Identifying $22 billion in spending reductions from the Federal Highway Administration budget would not be an easy task, especially if one anticipates needing 218 votes in the House and 60 votes in the Senate for a bill implementing those reductions. The following donut chart divides that funding into major programs and categories. This will give the reader a sense of the relative difficulty in identifying $22 billion per year in program reductions from this level.

[i] Congressional Budget Office. (2026, February). The budget and economic outlook: 2026 to 2036. U.S. Congress. https://www.cbo.gov/publication/

Mass Transit Account: Spending Cuts Needed for Solvency

For the Mass Transit Account, it is already too late to forestall insolvency by relying on future spending cuts alone. This is because the Mass Transit Account is more underfunded relative to authorized spending than the Highway Account. While CBO projects that highway account tax receipts will cover 65 percent of spending from the highway account for the next decade, for the transit account, the dedicated taxes will cover only 36 percent of spending.

Spending levels have already been set in law for fiscal year 2026—the final year of the IIJA. CBO estimates that the Mass Transit Account will reach a zero balance in mid-2027 and finish that fiscal year $2.7 billion in arrears. Add to that a $1 billion “cash cushion” to keep the Account from running dry on a day-to-day basis while awaiting twice-monthly tax deposits towards the end of the year, and FY 2027 outlays would have to be reduced by $3.7 billion to stave off insolvency.

However, the slow spend-out of mass transit programs means that the majority of outlays in 2027 will be for contract authority that was authorized two to five years previously, and unaffected by the level of new authorized obligation authority. The baseline amount of new obligation authority for Trust Fund transit programs in 2027 is only $14.6 billion. So with agencies converting only 10 percent of new spending authority into outlays in year one, the maximum reduction of new spending that could be achieved (e.g. by zeroing out all new obligation authority in FY27) would still only achieve a $1.46 billion reduction in outlays, which is less than half of the $3.7 billion spending reduction required.

The past underfunding of the Transit Account means it’s not possible to forestall insolvency by relying on future spending cuts alone

Even if you were to zero out all new Mass Transit Account spending starting in 2027, while still maintaining the existing revenues, the account would still need an estimated $8.5 billion bailout or revenue increase in 2027 in order to pay the bills incurred prior to 2027. Even with no new spending authority in the out years either, the account’s end of year balances would not start (i.e., become less negative) to grow until 2030.

Even more so than the highway program, the mass transit program funded out of the HTF is almost exclusively formula-driven, and the bulk of the money goes straight to hundreds of local governments. Identifying specific programs to cut quickly becomes politically problematic.

Resetting Distribution between Highways and Transit and Cutting to Achieve Solvency

Due to this imbalance between spending and receipts in the Mass Transit Account, the only way to close the shortfall by cutting spending, without new revenues or further bailout transfers from the General Fund, would be to reset the distribution of current tax revenues between the Highway Account and Mass Transit Account or to remove the distinction altogether.

Making the whole HTF solvent through spending cuts alone would require resetting the distribution between highway and transit accounts and reducing spending from both accounts by 48 percent.

We estimate that if Congress wanted to reduce funding to transit and highways sufficiently to close the deficit and to make those reductions at an equal rate, the highway and transit obligation limitation would both have to be reduced by 48 percent immediately. That’s the equivalent of a $30.1 billion first-year cut to annual highway programs and a $7.0 billion first-year cut to annual transit programs. This $194 billion reduction to new spending commitments over five years would save $129 billion in outlays by the end of 2031, narrowly averting insolvency at baseline tax revenues.

Part 5: Closing the Trust Fund Gap by Increasing Federal Revenues

The amount of federal spending on infrastructure has increased in nominal dollars to keep pace with the costs of infrastructure construction, which have increased with inflation. Spending also expands as priorities expand and transportation agencies take on additional missions and requirements. Maintaining the current set of missions and programs with neither cuts nor bailouts will require new revenues to the Highway Trust Fund. This section considers three options that predominate in current discussions. Importantly, each would raise its own issues with regard to collection and distribution.

Considerations

Collection and Administrative Costs:

Collecting revenues has some costs to it, but the percent of those costs relative to the amount of revenue collected can vary considerably. In general, increasing the rates of existing revenue streams will not add any new administrative costs and therefore will make the percent of costs going to administration go down. Creating new collection systems have higher costs.

Revenue systems can also vary based on the extent to which they will be prone to “leakage,” or the amount of unpaid revenues due to tax evasion or loopholes. A smaller number of taxable entities contributes to both low administrative costs and low rates of leakage.

Distribution Effects:

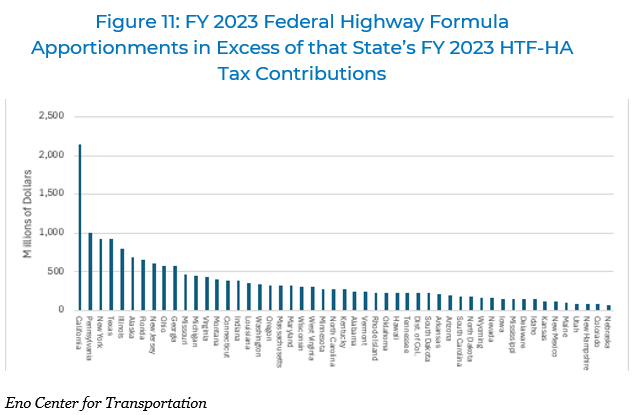

On the transit side, HTF dollars are distributed in amounts calculated according to formulas set in law, which are based on population as well as transit system factors such as passenger miles and revenue miles. Highway “formula” funding is no longer truly a formula with distribution based on any system factors. Instead, funds apportioned to states are based on the percentage of the national total that they received in 2009, and they are only re-adjusted if a state receives less than 95 percent of their payments into the highway account.

When highway funds are highly supplemented with General Fund transfers, then all states receive more than they remit in taxes and therefore no state is a “donor” to the HTF. Adding new revenues to the Highway Trust Fund and achieving solvency could result in a “donor-donee” fight that has not really been seen since apportionments began exceeding revenues and the formulas were locked. Even without intentional adjustments to distribution “formulas”, increasing revenues would result in adjustments to the amounts that states receive because more states would trigger the 95 percent guarantee provision in law that stipulates that states receive an apportionment amount equal to at least 95 percent of the amount the state paid in revenues to the HTF. The upward adjustments to the states that have paid more in taxes results in a downward adjustment to the apportionments of all other states.

Achieving solvency could be an opportunity to update apportionments to reflect changes in population and driving patterns that have occurred in the past twenty years. Politically, it would be likely be easiest to renegotiate formulas in the context of increasing spending as well as revenues, as that would make it possible to update formulas and still avoid any state receiving a smaller apportionment than they received in the prior year. If new revenues backfill the current shortfall without any increase to total spending, then any change to the distribution of HTF dollars would result in winners and losers.

Economic concerns

Economists make two points about modeling user taxes or fees. First, if you increase an excise tax or fee on an item or activity high enough, you will depress demand for the item being taxed to some degree and push down the yield (what economists call elasticity of demand). However, motor fuel has been shown to be particularly resistant to elastic demand changes, at least at the price increase rates we will consider here, and driving is such a commonplace and necessary activity that it has been shown to be remarkably inelastic as well.

Second, any increase in excise or payroll taxes, or a user fee, means that someone, somewhere, has less net income to declare on their taxes, and therefore any excise or payroll tax increase will cause some amount of decrease to federal income tax receipts. CBO and OMB formerly rounded this off to 25 cents of reduced income tax receipts for every dollar of increased excise or payroll taxes. Since the 2017 tax cuts, this level has fluctuated by year, and is around 26 or 27 cents per dollar of increased excise or payroll taxes. This would not make a difference to the Highway Trust Fund itself, which gets credited with the gross amount of any increased revenue, but it does affect larger federal budget issues

Options to Raise Revenue

I. Increase and Index Current Revenues

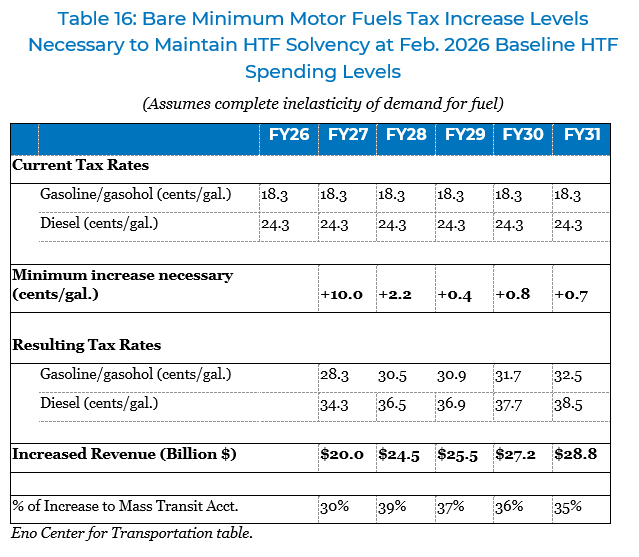

In the near term, CBO says that each penny of the 18.3 cent-per-gallon gasoline tax will bring just under $1.6 billion per year into the Highway Trust Fund, and each penny of the 24.3 c.p.g. diesel tax will bring in just over $400 million. This means that if Congress were to increase those motor fuel tax rates, each penny of rate increase would bring in an additional $2 billion per year to the HTF on a net basis.

We calculate that the bare minimum motor fuels tax increase necessary to maintain bare minimum Highway Trust Fund solvency at baseline spending rates is around 17.8 cents per gallon, starting with an immediate 10.0 cents per gallon on October 1, 2026 and increasing slightly each year thereafter. At the gradual increases calculated, the increase to fuel taxes would reach 14.2 cents by FY31 and would reach the full 17.8 additional cents per gallon by 2036. This would raise around $300 billion in additional tax revenue over ten years to the HTF (ignoring the income tax revenue lost because of the excise/payroll offset). Because of the imbalance between the leverage ratios in the two accounts, it would be necessary to give the Mass Transit Account over 30 percent of the increased revenues in the early years.

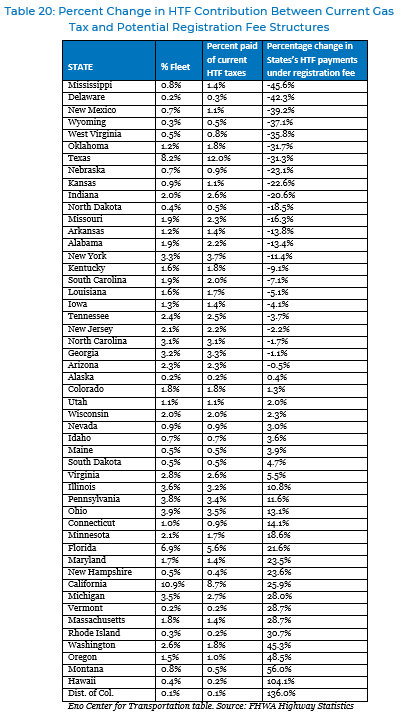

II. New Federal Annual Registration Fee

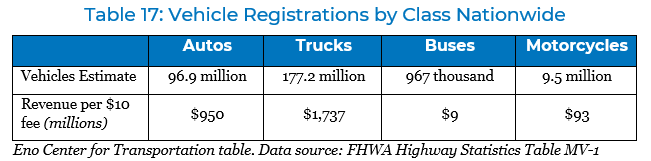

With roughly 300 million vehicles registered across the nation, a fee per registered vehicle has the potential to raise significant revenues. Even with two percent of revenues allocated for the cost of collecting revenues, a vehicle registration fee has the potential to raise approximately $2.8 billion for every $10 of registration fee imposed.

A federal registration fee offers a range of advantages and drawbacks. Chief among the advantages is the high potential revenue. While not a user fee, and a weaker proxy for use of roadways compared to the fuel taxes for internal combustion engine vehicles, it would capture the growing number of electric and alternative fuel vehicles. Therefore, the revenues would not erode should those numbers continue to increase.

The shortfall between current outlays and revenues is approximately $33 billion per year. At this level of spending, we estimate that a $120 fee on all vehicles would close the revenue gap. Alternatively, if Congress were to repeal all existing HTF revenues and replace them with a registration fee, a fee of $290 per vehicle would raise approximately $80 billion per year, covering the total HTF spending. (Congress could also consider pairing a higher fee on heavier vehicles that disproportionately impact roadways and a lower fee on smaller passenger vehicles, similar to the higher fuel tax rates for diesel fuel.)

The collection system poses the largest hurdle and disadvantage of a registration fee. All vehicles are required to be registered and have a title for the purpose of identification and demonstrating ownership, but the authority to register and title motor vehicles is a state authority. The federal role is limited to the licensing of U.S. government-owned vehicles and the registering of companies that operate commercial vehicles engaged in interstate commerce or passenger transport. The latter requirement, which mandates display of a USDOT number by interstate commercial vehicles, still does not supplant the requirement for state level vehicle registration.

A registration fee of $120 per year on all vehicles would fill the current HTF shortfall.

Federal vehicle registration requirements apply only to commercial vehicles over 10,000 pounds gross vehicle weight. There is no current federal registration for light-duty vehicles, and creating a wholly new system for administering federal registrations for the nearly 300 million vehicles in the country would impose a significant administrative cost burden. As a result, proposals for a federal registration fee generally assume that such a system would have to be layered onto the existing state-level systems for fee collection to keep administrative costs to manageable levels. Even so, integrating a new federal fee into disparate state collection systems would need to be carefully implemented, and the limits of state and federal authorities pose unique challenges.

Challenges and considerations:

Differences in State systems and requirements: All states require vehicles to be registered and licensed before being used on public roadways; however, registration practices vary greatly among states, including different registration renewal lengths (e.g. annual versus multi-year registrations), different fee structures and information collection systems, and different agency authorities.

Self-certification based on available information: State agencies typically rely on self-reporting of vehicle information; many states do not have vehicle inspection requirements and may not be able to confirm the accuracy of self-reported data. This may constrain the level of vehicle differentiation that could be included in a federal fee structure. For instance, fee amounts that vary based on vehicle weights could pose challenges for states to verify, as weights are not required to be tracked for passenger cars as part of Vehicle Identification Numbers (VINs).[i] For the categories of trucks and “multipurpose passenger vehicles”—e.g. SUVs, vans, and minivans—the VIN is required to include weight but in the form of gross vehicle weight rating class. This rating class is based on the vehicle weight plus total passenger and cargo weight that can be safely transported by the vehicle, rather than the weight of the vehicle itself. Similarly, fee differentiation based on fuel or propulsion type would be subject to self-reporting, as that information is not necessarily included in VINs.

Voluntary Structure: A federal requirement for state agencies to collect federal revenues would run afoul of the tenth amendment to the U.S. Constitution, which prohibits “commandeering” of state agencies. As a result, collection of these federal registration fees would have to be structured as a voluntary program in exchange for receipt of federal transportation program funds. Participation would likely also require authorization by state legislatures.

Ensuring State participation: If the registration fees were the sole source of revenues to support the transportation programs, then many states would find themselves collecting and remitting more funding than they received back as federal apportioned funds; this would undoubtedly dampen their willingness to voluntarily participate. The withdrawal of all “donor states” from a voluntary program structure would lead to the eventual collapse of the program.

In order to maintain full participation, a voluntary program would need ensure that states continued to see benefit in participating in the federal programs, which could be achieved in a variety of ways. States would have the incentive to continue participating if they were confident they would receive a greater amount of funding than they were collecting in fee revenue. For instance, the HTF could continue to be funded with additional revenues collected directly by the federal government such as fuel or truck taxes, and state receipt of the full apportionment could be conditioned on their participation in the voluntary registration fee collection. State eligibility for discretionary grants could also be conditioned in a similar way. Alternatively, regulatory waivers or other benefits could be provided only to program participants. Any of these approaches would require Congress to thread a needle of having an incentive that is significant enough to ensure participation but not so significant as to run afoul of the commandeering prohibition.

Stand-alone/supplemental fee on electric and hybrid vehicles:

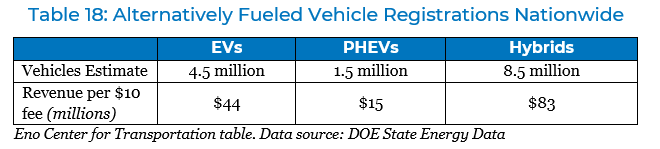

Electric vehicles do not consume gasoline and therefore do not contribute to the HTF through the gas tax; hybrids consume relatively little gasoline and contribute relatively little revenue. This has posed a concern to policymakers watching the total number of electric vehicles (EVs) and plug-in hybrid electric vehicles (PHEV) increase rapidly over the last decade, with the number of EVs and PHEVs growing at an average of 36 percent per year since 2016. However, the fact is that the total number of EVs and PHEVs remain an exceedingly small percentage of the overall vehicle fleet. As of 2024, EVs and PHEVs together represented just 2 percent of all vehicles, and non-plug-in hybrids represented another 3 percent.

Policymakers could impose a fee on EVs, PHEVs, and hybrid vehicles in addition to the base registration fee for all vehicles, or as a standalone new revenue to supplement current HTF revenues. A $200 fee on all of these vehicles, which is more than twice the average amount of federal gas tax paid by U.S. drivers, would still collectively raise less than $3 billion per year.[1] This would be a meaningful supplement to other sources of revenue, and one poised to potentially grow, but in the near-term, this revenue would be woefully inadequate to close the HTF revenue shortfall on its own.

A $200 fee on all EVs, PHEVs, and Hybrids would be twice as much as average gas tax payments but still only raise $3 billion per year.

Distribution effects:

Imposing a new federal fee or tax could be done independently from changes to funding apportionments, so there would not necessarily be any distributional effects. However, a new source of revenue would result in changes to the proportion of funding that each state receives relative to their taxes paid. This could create pressure to change the formula and also–depending on the fee level and amount of revenue paid—could result in new states triggering the minimum guarantee threshold of 95 percent of taxes paid.

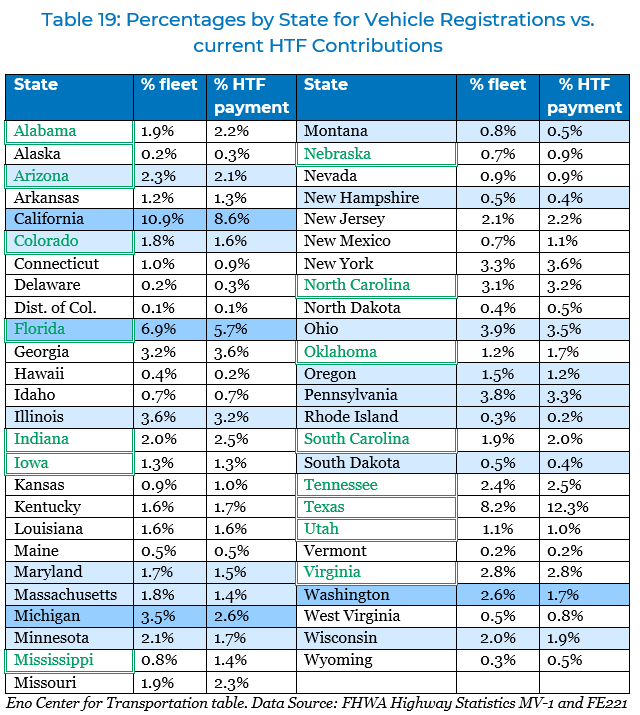

Due to the large increase in contract authority under IIJA provided through General Fund transfers, no state has received less than 100 percent of their tax payments in recent years, and the average formula apportionment in 2024 was 206 percent of the amount the state paid in HTF taxes. However, if a reauthorization bill relied solely on HTF tax revenues with no General Fund transfers, then many more states would trigger the 95 percent guarantee threshold.

The number of vehicle registrations has never been a factor used in state funding formulas, and therefore the states that were closer to being “donor states” previously would not necessarily be the same as those who would pay more under a vehicle registration framework. (The number of vehicles is somewhat correlated with population and with vehicle-miles traveled however, both of which were previously factors in distribution formulas.)

The green lettered states in the table above received 125 percent or less of their HTF tax payments, meaning they are currently closer to being “donor” states. The states that are shaded blue are those states that have a higher share of the nationwide vehicle fleet than their share of the payments into the HTF, with the darker shading indicating a larger percentage difference. Those states would pay relatively more if fees are collected on the basis of numbers of vehicles registered, and would be pushed toward being “donor states”. As a result, the set of states that are both green lettered and shaded blue are the states that would be most apt to trigger the 95 percent guarantee threshold—Arizona and Florida.

Nearly all states would see in a significant difference between the amount of current HTF payments from their residents to the amount of payments based on vehicle registrations, but the effect will vary across states. Approximately half the states would pay more than they currently do and the other half would pay less. The change would be minimal for some states, but for others, it would represent a much more significant change. While the states of Mississippi and Delaware would see a 40+ percent reduction in their payments into the HTF compared to their payments under the current tax structures, the states of Washington, Oregon, Montana, Hawaii and the District of Columbia would all see increases of more than 45 percent.

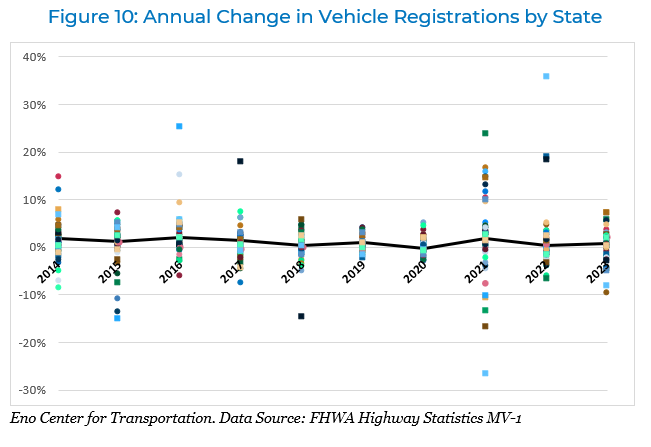

Future trends

Nationwide, the total number of vehicles generally increases on an annual basis. Between 2013 and 2024, the number of registered vehicles in the U.S. increased by an average of 1 percent per year. However, this overall average masks differences within states, and in 12 states, the number of registered vehicles in 2024 was lower than the number in 2013, with particularly significant reductions in the states of Alaska, Delaware, New York, and New Jersey. The figure below shows the percentage change each year for every state, each represented by a separate dot. While the national average—represented by the solid black line—shows steady annual growth, every year there are also numerous states that have negative growth in vehicle registrations.

[1] Assuming an average of 24 MPG fuel efficiency and an average of 12,000 miles, a driver would pay $92 in federal gas taxes in a given year.

[i] U.S. Government Publishing Office. (n.d.). 49 CFR Part 565—Vehicle identification number requirements. Electronic Code of Federal Regulations. https://www.ecfr.gov/current/title-49/subtitle-B/chapter-V/part-565

III. Federal VMT fee

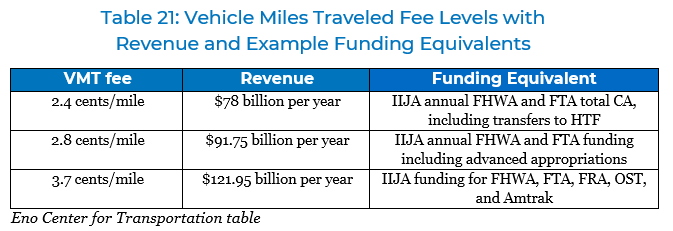

Vehicle-Miles Traveled fees have represented an area of promise for future HTF solvency for decades. In 2009, Congress established the National Surface Transportation Infrastructure Financing Commission to provide recommendations on how to fund and finance surface transportation infrastructure, and the Commission’s final recommendation was to shift from the current funding approach toward fees per mile driven.[i] VMT fees are appealing for several reasons, but perhaps two most important: first, by directly charging drivers per mile traveled, VMT fees would be true user fees, unlike fuel taxes or vehicle registration fees that use other factors as a proxy for the use of roadways. Second, and most importantly, in a country that collectively travels more than 3 trillion miles per year, a very small fee per mile could raise significant revenue.

Our calculations suggest that a per mile fee of 2.4 cents would raise the equivalent of the full amount of annual outlays for highway and transit programs per year. Imposing a VMT without removing the existing HTF taxes would necessitate a VMT of half that amount. A higher per mile fee would produce revenue sufficient to address the infrastructure priorities that were paid for through advance appropriations in IIJA.

Challenges and Considerations:

Multifactor Pricing potential: The 2009 Commission argued that VMT fees would not only restore the HTF finances, but they could also address the underpricing of roadways that results in congestion.[i] VMT fees could be structured as dynamic multifactor prices that would more completely reflect the full costs imposed by driving by having fees vary according to vehicle weight or emissions, time of day, congestion, location or other impacts.

Concerns: While VMT fees continue to be studied and have been implemented in some states, public concerns about VMT fees have also been widespread. These include concerns about privacy, cost impacts, unfairness to drivers of fuel-efficient vehicles, unfairness to drivers in rural areas, and others.[ii] Concerns about both implementation technology needs and privacy have led some RUC programs to embrace a range of payment options, giving drivers a choice to use paper-based system or in-vehicle technology. However, maintaining a range of collection systems only increases the administrative cost challenges.

Administrative Costs: Perhaps the most significant challenge is the administrative costs of collecting VMT fees. A pilot program to evaluate administration of a federal VMT fee was authorized in IIJA but never implemented. New Zealand has a Road Usage Charge (RUC) system currently in place for light-duty electric and diesel vehicles, which costs 3 percent of revenues to administer, compared to 0.04 percent cost for the country to administer the excise tax on fuel.[iii]

Tracking and Collection Technology: The NZ RUC program uses a mix of paper-based compliance and electronic distance recorders to track mileage. However, this system is what contributes to the very high administrative costs and poses challenges to enforcement and compliance. Smart phone applications and in-vehicle telematics offer the potential to lower administrative costs, though such systems would likely require opting in and would not be options for all vehicles. Beyond posing higher costs, manual systems do not support dynamic multifactor pricing.

A fee of 2.4 cents per mile would raise the equivalent of the full amount of annual outlays for highway and transit programs per year.

Distribution effects:

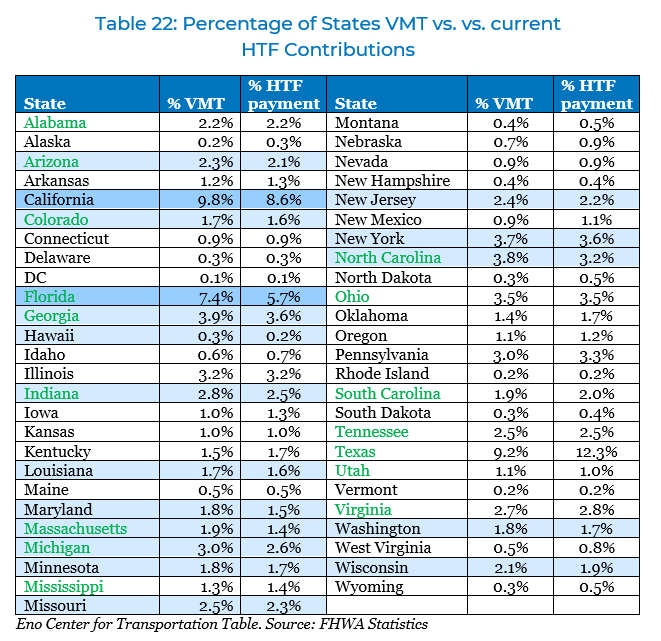

The blue shaded states in Table 22 are those for which their share of nationwide VMT is higher than the share of HTF payments they currently make. VMT is highly correlated with the amount of fuel used and, therefore, gas tax paid. As a result, many of the states that are already closer to being “donor” states on the basis of the taxes paid to the HTF (those states with green letters in the table below) would continue to be pushed toward being donor states if revenues were collected based on VMT and apportionments were not adjusted.

Future trends:

The nationwide average trendline for VMT growth stays largely steady from year to year, growing at an average of just under one percent per year since 2015, although national VMT is highly correlated with the economy and shrinks during economic recessions. However, that national average masks significant variation between states. Even excluding 2020 when every state saw negative VMT growth due to the COVID-19 pandemic, between 2015 and 2024 at least 9 states every year saw a reduction in their VMT from the prior year, and there are 12 states whose total VMT was actually lower in 2024 than it was in 2015.

[i] National Surface Transportation Infrastructure Financing Commission. (2009). Paying our way: A new framework for transportation finance (Final report). https://rosap.ntl.bts.gov/view/dot/17160

[ii] National Academies of Sciences, Engineering, and Medicine. (2016). Public perception of mileage-based user fees. National Academies Press.

[iii] New Zealand Ministry of Transport. (n.d.). Transitioning to road user charges: Initial decisions. https://www.transport.govt.nz/assets/Uploads/Transitioning-to-Road-User-Charges_-Initial-Decisions_Redacted.pdf

[i] National Surface Transportation Infrastructure Financing Commission. (2009). Paying our way: A new framework for transportation finance (Final report). https://rosap.ntl.bts.gov/view/dot/17160

Part 6: State Revenues and Devolution

The Federal-aid highway system today is federally-assisted and state-administered; similarly, transit agencies receive federal funding, and the local agencies select and deliver projects, and operate the assets supported by those funds. With federal assistance comes a bevy of federal requirements, notably compliance with regulations that affect procurement, domestic content, design and engineering specifications, location choices, environmental mitigation, and other outcomes. The federal program structure also sets constraints for state and local agencies. For instance, the total amount of each state’s apportionments for highway programs versus transit is set by law, as are program levels within each mode. These laws determine the amounts available for various project types (although at this point there is a fair amount of flexibility to transfer funding between programs and modes).

History of the Federal Programs

The original 1956 highway law more than tripled annual funding levels for the Federal-aid highway program and provided that, after the construction of the new, 41,000-mile system of divided, limited-access Interstate highways was completed, the Highway Trust Fund would be abolished, and Federal-aid funding and related taxes be reduced back to their pre-1956 levels. Whether or not this outcome was the actual intent of the authors of the 1956 law, they at least wanted to ensure that future Congresses would have to debate the issue of whether or not to extend a super-sized Federal-Aid Highway Program, post-Interstate.

Congress has consistently extended the authorization of the Highway Trust Fund starting in 1970, but there have also consistently been voices arguing to devolve the federal collection and distribution of funding for transportation. Devolution proposals would repeal (or more often reduce) the federal HTF revenues measures and prompt states to replace that federal funding with alternative state revenue measures. Devolving the funding would enable states to also avoid the regulatory compliance costs and legal constraints imposed by the federal programs.

In the 1980s, the U.S. Advisory Commission on Intergovernmental Relations (USACIR) critically examined the potential to devolve the highway and transit programs. With 97 percent of Interstate system already complete and the majority of costs for the uncompleted portions associated with projects that lacked national significance per CBO, USACIR recommended devolution of the highway and transit programs.[i] Many of the findings of the USACIR report still appear relevant. “Simultaneous devolution of a federal responsibility to states and localities along with the relinquishment of a federal revenue base to finance that responsibility” would help to stabilize the financing of highways according to the report. Moreover, “with state and local governments freed from federal requirements, some of which are unsuitable and expensive, turnbacks offer the possibility of more flexible, more efficient, and more responsive financing of those roads that are of predominantly state or local concern. Investment in highways could be matched more closely to travel demand and to the benefits received by the communities served by those roads.”[ii]

Throughout the years, Members of Congress have proposed devolution in stand-alone bills and as amendments to surface transportation laws. Such proposals have typically taken one of two forms. One model of devolution is based on the recommendations of USACIR: reduce federal excise taxes, allow states to opt to raise those taxes instead, and limit federal activity to core federal functions (such as roads on federally-owned lands and, possibly, maintaining key standards on the Interstates). The Transportation Empowerment Act of 1996, introduced by Representative John Kasich (R-OH) and Senator Connie Mack (R-FL), was the first legislative proposal of this form.[iii] The second form of devolution is structured as an opt-out option for states paired with the rebating of HTF contributions to states that choose to opt-out. This idea was first introduced by Senator Kay Bailey Hutchinson (R-TX) in the Highway Fairness and Reform Act of 2009.[iv]

In the short-term, devolution would not be an immediate no-cost solution to Highway Trust Fund shortfalls. As noted in Part 3, there is a buildup of outstanding obligations from the HTF for which the federal government is already legally responsible.[1] Between the $86 billion of obligated balances and the $44 billion in unobligated spending that was previously authorized, the USDOT authority would likely face the need to defray a total of $130 billion of unpaid bills at some point in the future. The current HTF balance of $74 billion would cover a portion of this, leaving $54 billion in additional future revenue needed to cover USDOT’s legal obligations. In other words, Congress could devolve and zero out the current programs but would need to extend current HTF taxes for another eighteen months, post-devolution, in order to raise the requisite funds. Since most states would need to increase their own tax revenues immediately, this could result in a period of double taxation which could be difficult for elected officials to explain and justify. Alternatively, a devolution plan could provide yet another transfer from general revenues in order to pay off validly incurred federal obligations from the pre-devolution days.

Serious consideration of devolution would also require Congress to determine which functions require a federal role, whether there is a continued need for federal standards, and how to fund NHTSA and FMCSA, which both receive funding from the Highway Trust Fund.

Despite these questions and obstacles, there may be real benefits of a new conversation on devolution as a means of improving the relationship between transportation improvements and the communities they serve. Federal funds support a range of activities that are not inherently federal in nature. While they still predominantly fund large-scale capital improvements on the National Highway System, many of the community projects may be more appropriately funded at the state and local level. Moreover, the federal program priorities may push states toward expansion projects versus maintenance work.

It is also difficult for national standards to adjust to different geographic conditions and land-use patterns. Inflexible federal design standards have led to roads with overly large rights of way, increasing land acquisition and construction costs and creating unique challenges in dense environments. As the USACIR report noted, “the design standards in federal law or regulations… can force the construction of a road that is more costly because it is built to a higher level than is needed or justifiable in terms of budget priorities.”[v]