Mending or Ending the Highway Trust Fund – the Great Debate of 1978

September 14, 2018

Last week’s ETW study of how the Highway Trust Fund first went bankrupt (ten years ago this month) found that the main culprits were a decision made by Congress in 2002 to completely disconnect spending levels coming from the Trust Fund from the levels of revenues flowing into the Trust Fund, and the decision by the authors of the 2005 surface transportation authorization law to keep those unsustainable spending levels going and “spend down” anticipated Trust Fund balances so that they would hit zero shortly after the expiration of the authorization period. The latter was done in the hope that a future Congress would be forced to raise taxes in order to keep the spending going.

It is, therefore, a nice coincidence that this year is also the 40th anniversary of the first attempt by the House transportation committee to “spend down” Trust Fund balances to zero, and of a competing plan to ensure that annual Trust Fund spending commitments could never exceed annual revenues (which would, of course, have prevented the Trust Fund from ever going broke).

The story of the 1978 surface transportation bill had it all – conflict between House committees, conflict between the House and Senate, conflict between the Administration and Congress, last-minute veto drama, and even basic disputes as to how much money was in the bill. But what made that reauthorization cycle unique was a proposal to fundamentally reform the way the Highway Trust Fund worked.

A word on accrual accounting. Part of this story revolves around the difference between two kinds of accounting. (Bear with me before your eyes glaze over.) This recent Congressional Budget Office report sums it up:

Transactions in cash-based accounting are recorded when payments are actually made or receipts collected. By contrast, accrual measures summarize in a single number the anticipated net financial effects at a specific point in time of a commitment that will affect federal cash flows many years into the future. That is, accrual methods record the estimated value of expenses and related receipts when the legal obligation is first made rather than when subsequent cash transactions occur.

Most of the federal budget uses cash-based accounting and always has. The federal deficit or surplus is measured by comparing the cash coming in the door (tax receipts, user fees, etc.) with the cash going out the door (outlays). The big exception, since 1990, is federal credit programs, where the eventual net total cost to the federal government of the loan, over 30 years (or however long the loan life is), is booked at the time the loan is made. When the federal government makes a TIFIA loan, for example, that nine-figure check written to a state or locality is not recorded as a federal outlay – only the estimated lifetime net cost of the loan gets recorded as an outlay.

(Interestingly, the 1967 President’s Commission on Budget Concepts recommended in its final report that the federal government switch over from cash accounting to accrual accounting for expenditures. The recommendations of the Commission are generally regarded as holy writ by CBO and OMB, but Presidents Johnson and Nixon delayed the implementation of accrual accounting because the Pentagon said they needed more time, what with the Vietnam war and all, and the issue was later dropped.)

The difference between the two types of accounting systems gets clearer when you look at spending commitments that take a long time to “spend out.” Under cash-based accounting, if Congress increases highway spending by $1 billion in 2018, only about $250 million of that money shows up as an expenditure (outlay) from the Highway Trust Fund in that year. The rest of that $1 billion can take six or seven years to “spend out” fully. But if the Trust Fund operated under accrual accounting, the full $1 billion would be booked in the Trust Fund in 2018 and would be measured against future scheduled Trust Fund tax revenues.

Cash versus accrual also makes a huge difference when conceptualizing the balance of a trust fund account. Cash based accounting looks at the cash balance of a trust fund at any given time. But accrual accounting looks at the unobligated, or uncommitted, balance. This is critically important – what looks like a huge cash balance can, in fact, be mostly or entirely obligated for specific programs and projects already and is simply awaiting outlay. Just because cash is sitting in a trust fund does not mean that the money is available to pay for new spending commitments.

Jimmy Carter and Brock Adams. The 1976 Presidential election sent Jimmy Carter to Washington, where his party would have control over a unified federal government for the first time in eight years. In the Congressional elections, Democrats won 292 seats in the House (just over two-thirds) and 61 seats in the Senate (enough to shut down filibusters). In terms of momentum and sheer numbers, the 95th Congress had the potential to be as game-changing as the Great Society Congress of 1965-1966.

For his Secretary of Transportation, Carter chose 12-year incumbent Congressman Brock Adams (D-WA). Adams had been a member of the Interstate and Foreign Commerce Committee and its Subcommittee on Transportation and Aeronautics, which had jurisdiction over railroads, the economic regulation of interstate trucking, and (until January 1975) over aviation as well. But also, from 1975-1977, Adams had been the first real chairman of the House Budget Committee. (Al Ullman (D-OR) had been chairman from August-December 1974 but the panel wasn’t really going then.) As such, Adams had been a key participant in the establishment of the new Congressional budget process and was one of the main advocates of giving the new Budget Committees an important role in forcing other Congressional committees to keep their spending within the bounds set by the budget resolution.

Adams took several Budget Committee staffers with him to USDOT, including Mort Downey, who had been the Budget Committee’s original transportation analyst and who became Assistant Secretary for Budget and Programs at USDOT.

The new Budget Act had also set a ticking time bomb counting down in surface transportation. Up until that point, both the federal highway and mass transit programs were funded by multi-year contract authority provided in authorization acts. The highway contract authority was paid from the Highway Trust Fund, and the mass transit contract authority was paid from the general fund. A key feature of the Budget Act of 1974 was its ban on new “backdoor spending,” which included general fund contract authority. After the Budget Act was signed into law (but before it took effect), Congress enacted a huge lump sum of mass transit contract authority from the general fund in November 1974 that was supposed to be enough to tide transit programs through 1979, but after that, the program fell off a cliff. The future outlook for multi-year mass transit funding was uncertain.

Transportation was far from the top of President Carter’s agenda (aside from a handwritten note he sent Adams two months after his inauguration suggesting that new subway systems were a waste of money). The energy crisis and the struggling economy were front and center. In a January 24, 1977 outline of the Carter Administration legislative agenda for its first year, here is all that was said about transportation (the handwritten emphases were put there by Carter himself):

![]()

Starting in April 1977, Adams developed a plan to use some of the new energy taxes being discussed as part of the President’s energy plan as a “pay-for” for mass transit and railroad (principally Amtrak) grant programs that were currently being funded out of the general fund, which were totaling about $4.5 billion. In a memo to the President on July 15, Adams proposed putting the receipts from the tax increase, along with the existing Highway Trust Fund taxes, into a new “National Transportation Account” to cover highways, transit, rail and airport grant programs.

Adams wrote that one big multi-modal fund would “generate a secure funding mechanism broad enough to support not merely the narrow interest of any single mode, but the competing interests of all transportation modes” and would “jointly evolve an approach whereby major programs could be reviewed systematically, allowing broad considerations of trade-offs, relative needs and basic program merits to be assessed, rather than looking at highways one year, UMTA another, and railroads still another.

Carter’s advisors opposed Adams’ plan. White House energy czar Jim Schlesinger and the Treasury Department said that diverting the energy taxes to a specific program would damage the energy plan, and Stu Eizenstat, Carter’s domestic policy chief, was against dedicating any specific taxes to specific programs, stating that “Our experience with the Highway Trust Fund illustrates that such earmarking creates a floor rather than a ceiling on these public works investments.”

The House decided in late July 1977 to bring the energy tax bill to the floor and, unusually, they allowed certain amendments to be offered to the tax title of the bill. House Highway Subcommittee chairman Jim Howard (D-NJ) offered an amendment to increase the gas tax from 4 cents per gallon to 9 cents per gallon in order to pay for a transportation bill he wanted to write the following year. The 5 c.p.g. increase would be split in half, with 2.5 cents to the Highway Trust Fund and the other 2.5 cents to a new mass transit fund. Brock Adams notified President Carter the following day that “This will be very difficult to pass because there is substantial opposition to a gasoline tax on the Hill. Clear support for the 5¢ tax from the Administration could be a critical factor. Unless you have further instructions, I intend to stress that the Administration does in fact favor the House leadership position.” But a diffident Carter wrote “I prefer more flexible use of the money” on Adams’s letter.

When the bill (H.R. 8444, 95thCongress) reached the House floor (sans gas tax increases) in August, Howard offered the 5 c.p.g. gas tax increase split 50-50 between highways and transit (starting on page 26997 here). President Carter gave a somewhat tepid endorsement: “While I initially recommended a standby gasoline tax which would provide a specific disincentive on the wasteful use of gasoline, or a gasoline tax with greater flexibility for use of the revenues, I recommend positive action on this proposed tax which is supported by the House leadership.”

But Howard’s amendment – a surface transportation user tax in the context of energy legislation, not transportation legislation, and therefore lacking any guarantees of additional transportation spending – failed by a huge 82 to 339 margin. Then, Rep. Dan Rostenkowski (D-IL) offered another amendment that would have imposed a smaller, 4 cent per gallon gas tax increase, which failed by an even wider margin, 52 to 370.

By November 1977, Adams and DOT had developed a full-fledged highway and transit reauthorization proposal, which Adams forwarded to the Office of Management and Budget for clearance. By that time, Adams had abandoned his plan for one big multi-modal fund, but the unfunded nature of mass transit was still a problem, so Adams wrote to the President that:

I propose the establishment of a public transportation trust fund for transportation programs that would relieve the pressure on general revenues with user-related taxes on petroleum. A fund based on energy taxes would provide a firm financial basis for carrying out these transportation programs, and the revenues would offset the expenditures in order to remain within budget targets.

-Transportation Secretary Brock Adams, November 11, 1977

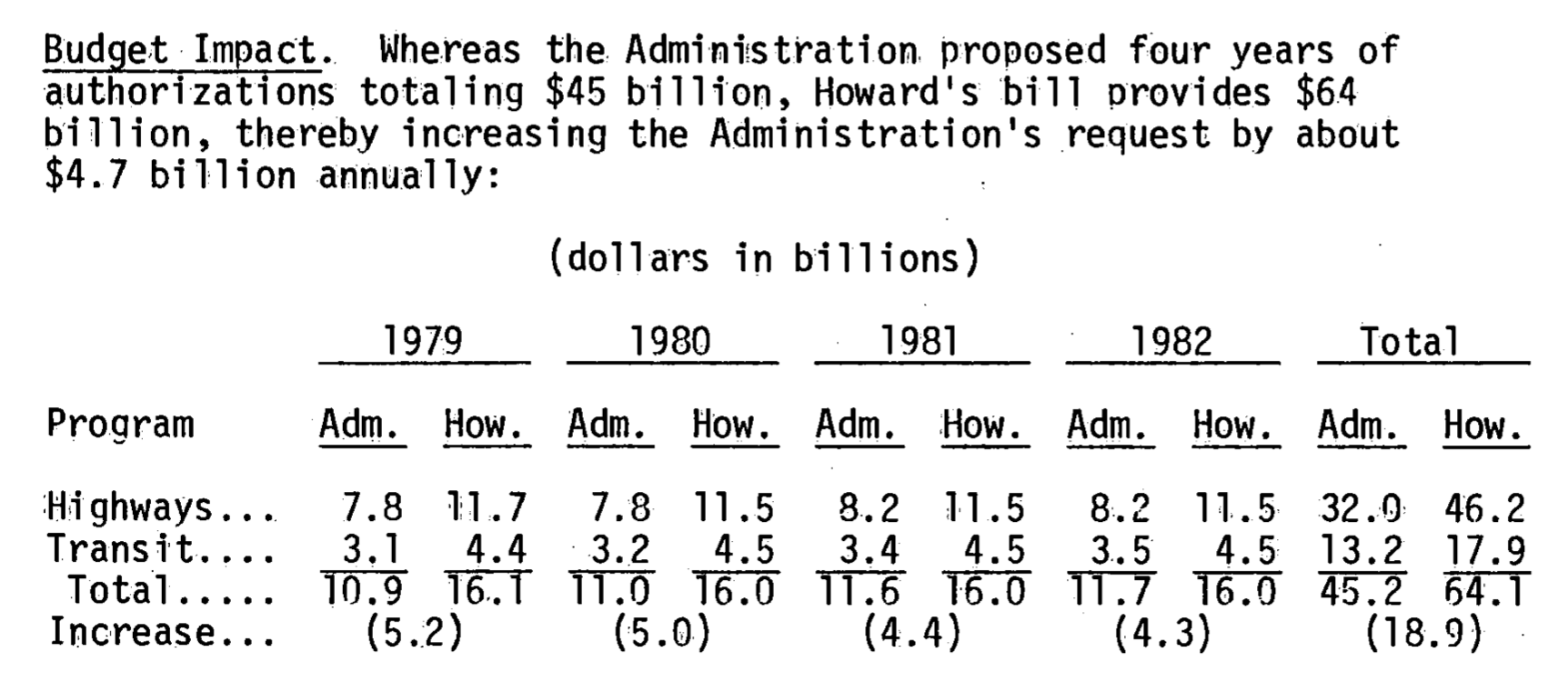

This plan was rejected by the White House. When President Carter formally submitted his Administration’s surface transportation in January 1978 (see page 1014 here), the legislation (introduced in the House by request as H.R. 10578, 95th Congress) made no changes to the Highway Trust Fund, and the bill’s mass transit authorizations made in that bill were simple general fund authorizations, subject to the whims of the Appropriations Committees. The bill proposed $32.2 billion in HTF contract authority over four years, an annual average that was 10.5 percent above the FY 1978 enacted level.

Source: Joint Committee on Taxation, JCS-5-78, February 8, 1978.

CBO tries to lead the debate. The 1974 Budget Act also created a new Congressional Budget Office to give Congress unbiased advice and expertise on budgeting. Under its first director, Alice Rivlin, CBO didn’t just try to be a scorekeeping body that analyzed bills and added up their costs – CBO also tried to act as a kind of in-house think tank for Congress.

In February 1977, CBO published an in-depth look at the mass transit financing problem, and in October of that year they released a detailed study of energy use by different modes of urban transportation. As the reauthorization of the highway program loomed, in February 1978 they released a detailed historical study of federal highway program funding.

Then, in March 1978, CBO decided to aggressively frame the surface transportation debate by publishing Transportation Finance: Choices in a Period of Change. Written by Dick Mudge and Porter Wheeler (under the supervision of future Eno Transportation Foundation head Damian Kulash), the report analyzed four different options for future funding options:

- Status quo (highways funded from the Highway Trust Fund, airports from the Airport and Airway Trust Fund, everything else from general revenues).

- A unified trust fund for all transportation modes, along the lines of what Brock Adams had proposed the previous year.

- Separate modal trust funds (the existing HTF and AATF, plus “new trust funds would be established for the other modes: a mass transit trust fund; an inland water trust fund to cover the appropriate expenditures of the Corps of Engineers and the Coast Guard; a separate trust fund for international water transportation (including the programs of the Maritime Administration); and one or more trust funds for rail programs”).

- Abolish the trust funds and make all transportation programs subject to appropriation from general revenues.

The study looked at each of those four options from a variety of perspectives:

Transportation Financing Options and Their Performance With Respect to Selected Issues |

||||

| Status Quo | Unified Trust Fund | Modal Trust Funds | No Trust Funds | |

| Congressional Policymaking | Fragmented; intermodal coordination difficult; limited oversight of trust funds | Good intermodal coordination possibilities | Tends to institutionalize fragmentation; restricts oversight by virtue of liquidating appropriations process | Could enhance intermodal coordination; offers good opportunites for oversight |

| Funding Assurance to States and Localities | Adequate assurance for highways; future transit funding could use more assurance | Could present problems: the coordination advantages of this option imply low funding assurance to any given mode | Strong assurance | Highways and airways would lose assurance; other modes may be slightly better off |

| Congressional Fiscal Control | Poor control; most spending outside normal appropriations process | No control of overall transportation budget; good control of modal allocations | No short-run budgetary control | Good budgetary control, both by mode and for transportation total |

| Nondiscriminatory Treatment of Modes | Modes have unequal opportunity to adjust funding | Would facilitate intermodal allocation of resources | Modes have equal access but the structure inhibits intermodal adjustment | No built-in modal advantages; encourages balance |

| User-Pays Principle | Good for trust-funded modes; possibly unfair to certain groups of users | Poor by usual interpretation of user-pays principle; possibly justified by broad social interpretation of principle | Permits close adherence to user-pays principle | No necessary adherence to user-pays principle |

| Organizational Compatibility | Clumsy but operational | Full-scale implementation of this option is probably organizationally impossible at present | No special problems | Requires substantial change for highways and airways |

Source: Table 2 in Congressional Budget Office report Transportation Finance: Choices in a Period of Change, March 1978

The report concluded:

On balance, the no trust funds option is probably the most desirable, primarily because it both strengthens the policymaking role of the Congress and provides greater fiscal control.

-Congressional Budget Office, March 1978

Needless to say, the powerful highway lobby, on and off Capitol Hill, was not pleased.

House Public Works pushes for more money. On March 21, Secretary Adams met with House Highways Subcommittee chairman Jim Howard (D-NJ) and was informed that the bipartisan leaders of the Public Works Committee would shortly be introducing a bill that ignored the Carter Administration’s recommended budget totals and program reforms. Adams told Howard that, in that case, he would recommend that President Carter veto the bill. Howard told Adams that he would not mind a veto threat at all.

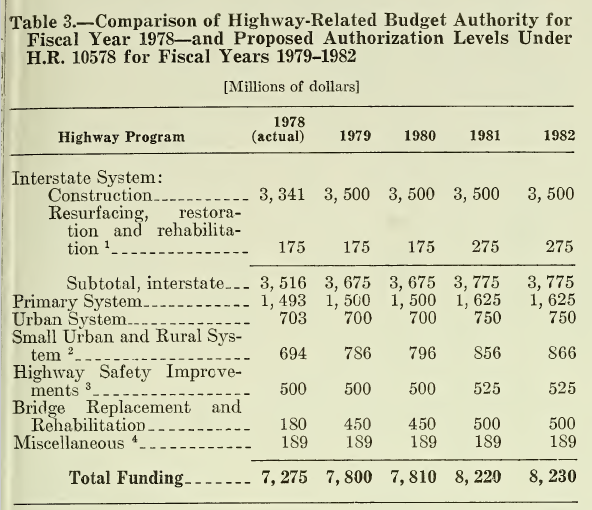

The following day, Howard, his ranking minority member on the subcommittee Bud Shuster (R-PA), and other bipartisan members of the Public Works and Transportation Committee introduced H.R. 11733 (95th Congress), an ambitious four-year reauthorization bill. The bill would have allowed a total of $44.5 billion in Highway Trust Fund contract authority over that period, an average of $3.1 billion per year more than the President’s request (40 percent above the President’s totals). The goal was to “spend down” the $10.2 billion cash balance that was held in the Trust Fund at the start of fiscal year 1978.

When mass transit authorizations from the general fund were included, the differences between the Administration bill and the House bill were even greater.

Jim Howard told reporters that the bill was “undoubtedly the most significant piece of transportation ever to come before” Congress. Jack Schenendorf, who was a young minority counsel on Public Works at the time, recalls that Adams was so angry at how little of the Administration’s bill made it into the committee’s bill that he held an impromptu press conference in the hallway outside the committee room denouncing Howard.

The White House recoiled. OMB Director Jim McIntyre sent President Carter a memo on April 4 opposing H.R. 11733 based on its substantial spending increases over the Administration’s request and its lack of program reforms. The memo recapped the Adams-Howard meeting of March 21 and said that “Administration relations with Mr. Howard and his committee have been severely strained…Chances of modifying H.R. 11733 in House Committee are dim. However, we concur with Secretary Adams’ position of trying to work with selected House Committee members who appear to be sympathetic to the Administration’s position. A more vigorous effort can be made on the House floor and the Senate.” The memo recommended a veto threat on H.R. 11733 from the White House.

White House staff secretary Rick Hutcheson forwarded the OMB memo to Carter with a recommendation from the White House domestic policy staff that the veto threat come through Adams, not the White House, and suggesting that Carter mention the highway bill as one of the big-spending bills opposed by the White House in a forthcoming Presidential speech on inflation. President Carter forwarded the OMB memo to DOT after handwriting “Brock – I’ll veto” on the front page and “Let Brock take lead, Frank [Moore, the White House legislative liaison] to help” on the decision box page.

White House staff secretary Rick Hutcheson forwarded the OMB memo to Carter with a recommendation from the White House domestic policy staff that the veto threat come through Adams, not the White House, and suggesting that Carter mention the highway bill as one of the big-spending bills opposed by the White House in a forthcoming Presidential speech on inflation. President Carter forwarded the OMB memo to DOT after handwriting “Brock – I’ll veto” on the front page and “Let Brock take lead, Frank [Moore, the White House legislative liaison] to help” on the decision box page.

Carter followed through on Hutcheson’s recommendations by making a note of the highway bill in an April 11 speech announcing the Administration’s anti-inflation policy: “Potential outlay increases in the 1979 budget which are now being considered seriously by congressional committees would add between $9 billion and $13 billion to spending levels next year. The price of some of these politically attractive programs would escalate rapidly in future years. I’m especially concerned about tuition tax credits, highway and urban transit programs, postal service financing, farm legislation, and defense spending. By every means at my disposal, I will resist these pressures and protect the integrity of the budget.”

Three days later, Jim Howard suffered a heart attack (his second) and the bill was put on hold for a time.

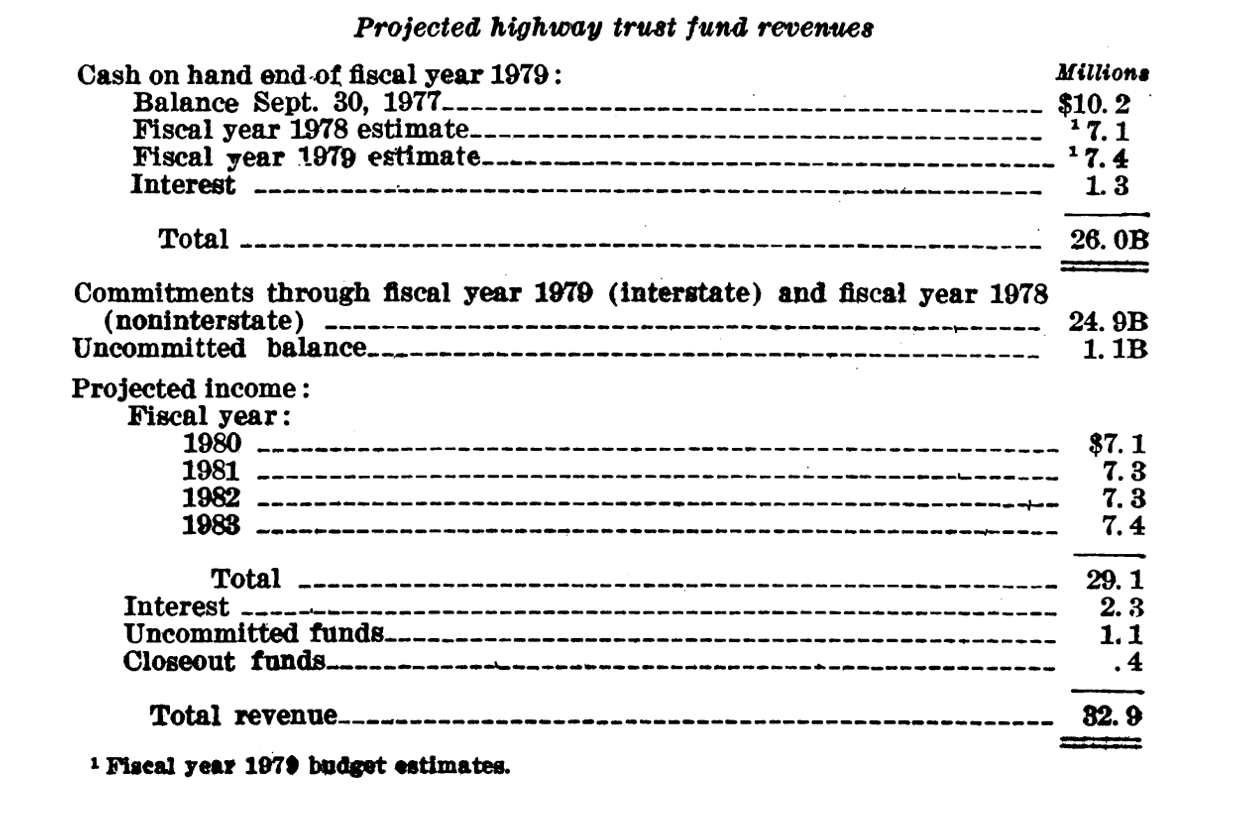

The push for accrual accounting. Although the Administration bill itself did not specifically reference accrual accounting, the general principle was on the mind of Secretary Adams when the bill was formulated. Adams made this clear when he testified before the House Ways and Means Committee on the proposed legislation on February 8, during which he said: “if everything works well, then the money coming in and the money that we have already authorized and already committed will just about balance.” Adams submitted a table for the record showing that the HTF estimated cash-on-hand at the end of FY 1979 would equal $26.0 billion and that outstanding commitments through the end of FY 1979 (for the Interstate program) and 1978 for other programs would total $24.9 billion, leaving an uncommitted balance of just $1.1 billion. Total HTF deposits for the FY 1980-1983 period were estimated to be $32.9 billion, and new authorizations in the Administration bill over the FY 1979-1983 period were $32.0 billion.

Mort Downey says that the accrual accounting concept was on his and Adams’s minds because of their shared experience on the Budget Committee in 1975, when New York City government ran out of money and needed a bailout. As part of the conditions that the Ford Administration (and Wall Street) set for the NYC bailout, an outside auditor (Arthur Andersen) had to come in and put the City’s liabilities on an accrual basis, instead of the mixed cash-and-accrual basis that was being used, so that the full size of the problem could be seen.

Knowing that the ultimate responsibility for the Highway Trust Fund and its solvency lay with the Ways and Means Committee, not the Public Works and Transportation Committee, Adams and Downey approached two Ways and Means members who had also served on the Budget Committee during Adams’s chairmanship – Barber Conable (R-NY) and Sam Gibbons (D-FL). The two legislators worked with DOT to conceptualize and draft an amendment to the HTF’s authorizing statute (at that time, it was the Highway Revenue Act of 1956 – the Trust Fund did not get added to the Internal Revenue Code until 1983) to put the Trust Fund on accrual accounting, which would have the effect of limiting authorization levels to anticipated revenue levels.

Senate and House highway markups. Interestingly, at this time, the Senate Environment and Public Works Committee was more fiscally conservative than the House Public Works and Transportation Committee. On May 11, 1978, the EPW panel approved its own highway title of a surface transportation reauthorization bill (reported on May 15 as S. 3073, 95th Congress in S. Rept. 95-833). It was a two-year bill providing just under $8 billion per year in new highway contract authority for fiscal years 1979 and 1980. The committee report said:

The committee firmly believes that future decisions on expenditures should be closely related to decisions affecting revenues. If the ‘user-pays’ principle is sound, it should be applied so as to assure that revenues from users are sufficient to cover program costs. Authorizations which clearly exceed revenues over a comparable time period lead to one of two consequences: (1) at some future time program levels will have to be drastically reduced because current revenues will be needed to pay for already-completed projects; or (2) in the future there will be an urgent need to increase revenues – that is, raise taxes – if severe program curtailments are to be avoided…Given the degree of State and local reliance on the Federal highway program, the first alternative appears unlikely. The second alternative is not desirable as it would require difficult revenue-raising decisions in a crisis context. Such an atmosphere is unlikely to produce a fair distribution of tax burdens and could well lead to efforts to use general funds as a way to avoid unpopular tax increases. Either outcome destroys the justification of a user-based trust fund.

-Senate Environment and Public Works Committee report, May 1978.

Meanwhile, House Public Works was marking up Howard’s bill at the same time, during a two-day session on May 11-12. Howard, recovered from his heart attack, managed the bill in committee. On the first day of the markup, Rep. Dale Milford (D-TX) offered an en bloc amendment cutting $8.4 billion in highway contract authority from the bill over four years and cutting general fund authorizations as well, to “reduce the proposed funding for highway and bridge programs to levels that will preserve the integrity of the Highway Trust Fund. Under these amendments, we will remain on a pay-as-you-go basis, rather than reverting to deficit spending. The amendment also makes reductions in proposed mass transit financing. With these reductions, the bill’s authorization levels will come closer to fitting within the Congressional budget allocations and should be more acceptable to the Administration.”

The Milford amendment fell woefully short, 7 ayes to 36 nays. After another day of markup, the committee ordered H.R. 11733 favorably reported on May 12. The reported bill authorized roughly $11 billion per year in new Highway Trust Fund obligations over four years, during which time HTF revenues were expected to vary between $8 billion and $9 billion per year. Under those projections, the bill would have spent the HTF cash balance down from $11.3 billion to $4.5 billion by the end of FY 1982, but would have set a trend under which the Trust Fund would have hit a zero balance two years later had those spending levels been maintained without a tax increase.

Because H.R. 11733 as introduced contained a tax title, the bill was jointly referred to Public Works and to Ways and Means, which meant that the bill could not proceed to the House floor and Public Works could not file its report until Ways and Means was ready as well. A Ways and Means markup session was scheduled for the following week, on May 18.

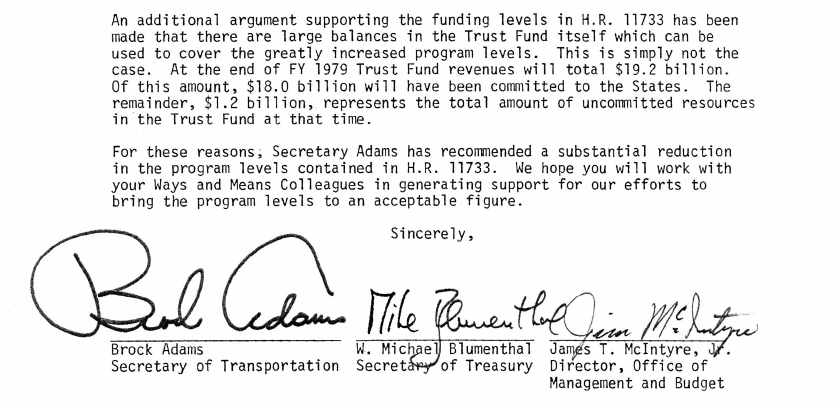

The Conable-Gibbons amendment. In its initial form, a May 16, 1978 draft of the Conable-Gibbons amendment to be offered in the Ways and Means markup recommended a form of accrual accounting, limiting total new authorizations to receipt levels. On May 17, the Secretary of Transportation, the Secretary of the Treasury, and the OMB Director wrote a joint letter to Ways and Means chairman Ullman in opposition to the spending levels in H.R. 11733, saying that the bill “does substantial violence to the concept of keeping program levels within projected revenues over an identical time frame.” The troika urged adoption of the Conable-Gibbons amendment, saying that “Without the Conable-Gibbons amendment, the Committee is faced with the unpalatable choice between imposing a 2 cent increase in the gas tax to generate the needed revenues or a depleted Trust Fund in the 1980’s.”

The letter also outlined the pivotal difference between the cash balance of the Trust Fund and the uncommitted balance.

As the scheduled May 18 Ways and Means markup of H.R. 11733 approached, it was abruptly postponed. A contemporaneous news account (in CQ Weekly Report on May 27) said that by May 17, Public Works had transmitted no information to Ways and Means about the bill except one copy of the version ordered reported, and quoted an anonymous Ways and Means aide as saying that “They might have been able to slip it through if they’d at least sent over a copy of the report.” The article then said that “Because no report language accompanied the bill, Gibbons and Conable asked Ways and Means chairman Al Ullman, D-Ore., to delay committee markup.”

On May 19, the chairman and ranking Republican of the full House Public Works Committee, Bizz Johnson (D-CA) and Bill Harsha (R-OH), wrote to Ullman to state their “firm opposition” to the Conable-Gibbons amendment, “which in our judgment would do considerable damage to the traditional and demonstrably productive relationship between the Highway Trust Fund and the Federal-Aid Highway Program.” Johnson and Harsha asked to present the Public Works views to Ways and Means at the appropriate time.

Five days later,Ways and Means held a second hearing on Highway Trust Fund issues, this time in the Subcommittee on Oversight, which was chaired by Sam Gibbons. The bill managers of H.R. 11733 from the Public Works Committee, subcommittee chair and ranking member Jim Howard (D-NJ) and Bud Shuster (R-PA), were invited to testify in person but sent a written statement instead. Transportation Secretary Adams and representatives from Treasury and OMB testified in person in favor of a version of the Conable-Gibbons amendment, as did the chairman of the House Budget Committee, Bob Giamo (D-CT).

The Director of the Congressional Budget Office, Alice Rivlin, testified:

The highway trust fund was established on the principle of pay as you go. Through this principle, which is embodied in policy statements contained in the 1956 legislation, the Congress established a procedure for keeping highway expenditures in line with highway taxes. This balance would be destroyed if the Congress were to authorize substantial new programs without providing for their financing. Within a few years, such a course of action would force the Congress either to raise highway taxes or to curtail programs sharply in order to rescue the highway trust fund.

-CBO Director Alice Rivlin, May 24, 1978

Later that day, the Public Works Committee issued a stinging press release attacking the Administration-backed Conable-Gibbons proposal as just another version of budget impoundment.

By May 31, the Public Works leaders were apparently regretting their no-show at the Ways and Means hearing. Chairman Johnson wrote to Ways and Means chairman Ullman saying that at the May 24 hearing, DOT, CBO and the Budget Committee “sufficiently confused the situation that it now becomes a necessity from my standpoint that the Committee on Public Works and Transportation come before your full Committee and present the factual situation surrounding our simple request for a Highway Trust Fund extension.”

Nothing happened immediately. On June 8, Gibbons’ subcommittee issued a report to the full Ways and Means Committee outlining the issues and summarizing the May 24 hearing, and laying out options for the full panel during its consideration of H.R. 11733. But no action was taken. By June 22, the Public Works leaders were getting antsy. Johnson, Harsha, Howard and Shuster sent another letter to Ways and Means chairman Ullman, this one saying that “We understand that Members of your Committee are being strongly urged to reject our financing approach in favor of a far-reaching restructuring of the Trust Fund mechanism. We therefore are writing now to urge you to avoid making a commitment to any such trust fund amendment until the Committee on Public Works and Transportation has had an opportunity to present its case.”

The letter was referring to the final version of the Conable-Gibbons amendment, which provided for automatic across-the-board reductions in highway apportionments if new Trust Fund authorizations were projected to exceed net receipts for the coming year.

The Ways and Means analysis of the amendment also drew a distinction between the existing Trust Fund self-sufficiency test (the “Byrd Amendment,” in place since 1956, which treated cash balances as being uncommitted) and the Conable-Gibbons proposal, which used the accrual accounting method of determining future liabilities:

The Byrd Amendment, which operates to keep the Fund out of a cash deficit position, would not become operative in time to effectively protect the fiscal soundness of the Trust Fund because the Fund presently has large cash balances. Although these balances are not “free” and in fact are already committed, these funds would be drawn down gradually to fund the higher program levels now proposed. This process would act to disguise the true condition of the Fund where commitments were outrunning available revenues by a substantial amount. Once this cash draw-down reached a point where it became obvious that the funds available were insufficient to finance the higher program levels, it would be too late to solve the problem except by a hurriedly enacted and massive tax increase or, in the alternative, by massive program cuts.

In order to prevent these drastic outcomes and unpleasant alternatives, it is necessary to maintain a reasonable balance between new authorizations and revenues available; this in turn will limit the amount of unfunded liabilities that can accumulate against the Trust Fund. The proposed amendment would provide these needed safeguards.

-Ways and Means staff analysis of Conable-Gibbons amendment, May 31, 1978.

On July 12, Public Works finally got its say, with Jim Howard testifying before a Ways and Means executive session in the morning. Howard got enough pushback so that he returned in the afternoon to announce that he would be amending H.R. 11733 on the House floor to reduce funding levels by $1 billion per year. (There was a period where Howard left Public Works staff director Dick Sullivan alone to argue with the Ways and Means members for what seemed like several hours). Even with the spending reductions, the Public Works bill would still spend HTF balances down from $11 billion in 1978 to less than $1 billion in 1990 if spending levels were frozen in place (no inflation adjustment) in perpetuity after the expiration of the bill.

Ways and Means finally started its markup session on July 31. White House OMB Director James McIntyre wrote to Gibbons to say that “the Administration believes that the highway authorization levels in H.R. 11733, even assuming the proposed $1.0 billion annual reduction, are still unacceptably high…Therefore, I want to reiterate the Administration’s support for the Conable-Gibbons Amendment or for any other measure which would lower highway and transit authorizations to levels more closely approximating those proposed by the Administration.” CBO also issued projections of HTF cash flow under the Conable-Gibbons amendment (on a cash flow basis, not an accrual basis) and under H.R. 11733 with the Howard amendment. But the votes did not appear to be there, and in the end, Conable and Gibbons did not offer their amendment during the committee markup. Ways and Means on August 1 approved a five-year extension of existing Highway Trust Fund taxes and expenditure authority, with no policy changes.

But the issue was not over – Conable and Gibbons would work with the chairman of the Budget Committee to offer an accrual accounting amendment to the highway bill on the House floor, in September 1978 (see part 2 of this article).

To be continued…