CP-KCS Merger Would Create Canada-US-Mexico Unified Railroad

In what seems like the last, unfinished piece of 1990s railroad merger mania, Canadian Pacific and Kansas City Southern announced on March 21 that the two railroads had agreed to combine. Canadian Pacific will pay $25 billion for the smaller railroad (valued at $275 per share, payable in CP stock) and will also assume $3.8 billion of KCS’s debt.

Kansas City Southern is by far the smallest of the U.S. “Class I” railroads, with $2.9 billion in 2019 operating revenues. Canadian Pacific had $7.8 billion in 2019 operating revenues, so the combined entity would be closer in size to CSX or Norfolk Southern.

Process. The merger is subject to review by the federal Surface Transportation Board, which by law must evaluate the proposed merger on whether or not the Board “finds the transaction is consistent with the public interest.” The specific grounds are laid out in 49 U.S.C. 11324. Since this is a merger of two Class I’s the more stringent procedures apply. The law requires the Board to consider at least five areas:

- the effect of the proposed transaction on the adequacy of transportation to the public;

- the effect on the public interest of including, or failing to include, other rail carriers in the area involved in the proposed transaction;

- the total fixed charges that result from the proposed transaction;

- the interest of rail carrier employees affected by the proposed transaction; and

- whether the proposed transaction would have an adverse effect on competition among rail carriers in the affected region or in the national rail system.

Notably, unlike most antitrust issues, the Justice Department’s view is not dispositive. The law requires the Board to “accord substantial weight” to the DOJ opinion, but in the 1996 Union Pacific-Southern Pacific mega-merger, DOJ urged the Board to reject the merger, but the Board ignored their recommendations and approved it anyway.

It should be noted that the current Board has a Republican majority (three GOP members and two Democratic members). Republican Ann Begeman is serving in her holdover period since her term expired on December 31, 2020. If President Biden nominates a Democrat and the Senate confirms the nominee, Begeman will be replaced immediately, but if no one is nominated, then Begeman’s holdover period ends on December 31 of this year and the Board drops from five members to four members on January 1.

Board composition is important because reviewing the merger of two Class I’s is a lengthy process and won’t be completed until 2022 at the earliest.

Until then, the money will change hands, but the two railroads won’t be functionally integrated. Per the joint press release:

First, CP will establish a “plain vanilla”, independent voting trust to acquire the shares of KCS. Upon shareholder approval of the transaction, and satisfaction of customary closing conditions, CP will acquire KCS shares and place them into the voting trust. This step is currently expected to be completed in the second half of 2021, at which point KCS shareholders will receive their consideration.CP’s placement of KCS shares into the voting trust will insulate KCS from control by CP until the STB authorizes control. KCS’ management and Board of Directors will continue to steward the company while it is in trust, pursuing KCS’ independent business plan and growth strategies.The second step of the process is to obtain control approval from the STB and other applicable regulatory authorities. The STB review is expected to be completed by the middle of 2022. Upon obtaining control approval, the two companies will be integrated, unlocking the benefits of the combination.

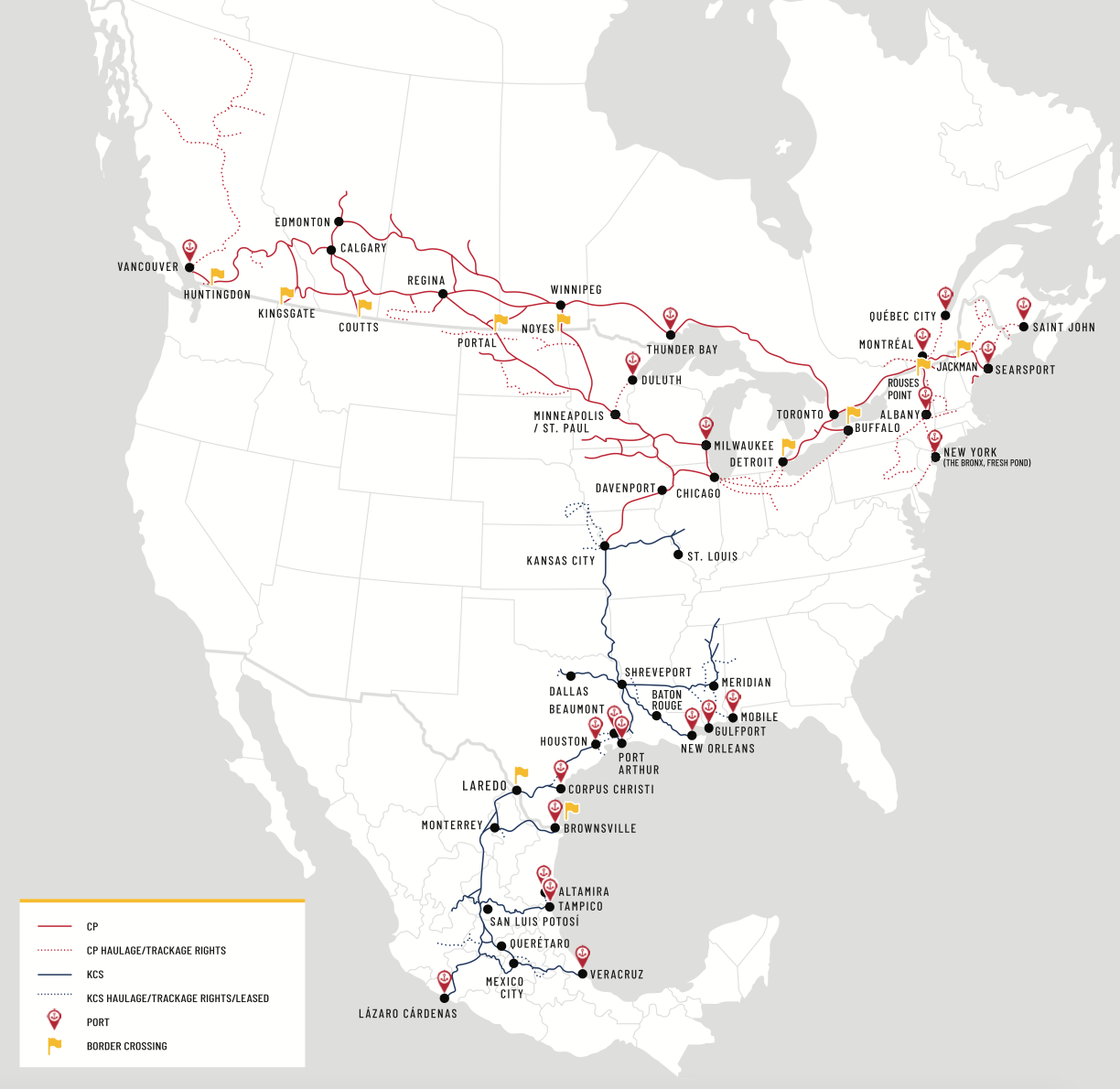

Advantages. The route map of the proposed combined railroad makes some of the advantages obvious – this would be a centrally owned and integrated Canada-U.S.-Mexico combined railroad, stretching coast-to-coast in the north (Vancouver to Saint John) and in the south (Lazaro Cardenas to Veracruz) with a north-south spine bisecting the U.S. in the middle, where cargo from the two western U.S. Class I’s and the two eastern U.S. Class I’s could be on- or off-loaded.

The two railroads have prepared other maps as well. One shows the location of automobile manufacturing plants to the new railroad (and almost all of the Mexican plants are centrally located in the KCS wheelhouse). One shows the flow of grain from the Canadian and U.S. Great Plains breadbasket areas to the grain-consuming areas of Mexico. And one shows the potential flow of energy products from the oil sands of Alberta and the Bakken range down to the refineries on the Gulf Coast.

This last one may answer the “why now” question on the merger – cancelation of the Keystone XL pipeline, and this Administration’s dim view of other new pipelines that would make it easier to extract oil from Alberta and the Bakken, strengthens the business model for transporting all that oil by railcar down to the refineries, which could be accomplished with this merger using a single railroad.

Merger background. Back in 1994, there were ten U.S.-owned “Class I” freight railroads, defined then as having annual revenues over $250 million. (There were also two other Class I’s operating in the U.S. as subsidiaries of Canadian railroads.) Over the next four years, mergers would cut the number of domestic class I freights in half:

| Atchison, Topeka and S.F. | bought by Burlington Northern in 1995 |

| Burlington Northern | |

| Chicago & North Western | bought by Union Pacific in 1995 |

| Conrail | split up between CSX and Norfolk Southern in 1998 |

| CSX | |

| Illinois Central | bought by Canadian National in 1998 |

| Kansas City Southern | |

| Norfolk Southern | |

| Southern Pacific | bought by Union Pacific in 1995 |

| Union Pacific |

As a result, for the last two decades, there have been four major U.S. freight railroads – two megacarriers operating mostly west of the Mississippi River (BNSF and Union Pacific), and two big carriers operating mostly east of the Mississippi (CSX and Norfolk Southern). And then there was one much smaller independent carrier, Kansas City Southern. BNSF and UP each do about twice the annual business that CSX and NS do, and the latter two still do almost four times the annual business of Kansas City Southern.

| 2019 Oper. Revenues (Billion $) | |

| BNSF | $23.1 |

| Union Pacific | $21.7 |

| CSX | $11.9 |

| Norfolk Southern | $11.3 |

| Kansas City Southern | $2.9 |

Meanwhile, up North, Canadian Pacific is the original transcontinental railroad in that country (built in the 1880s as a response to the U.S. completion of its first “transcon” in 1869, and also as part of the promise to get British Columbia to join Canada in 1871). The other Canadian transcon, Canadian National, is an odd example of how history runs at different paces in different countries. In the U.S., the major freight railroad bankruptcies happened starting in the late 1960s and resulted in the U.S. nationalizing a bunch of bankrupt railroads in the 1970s to form Conrail, which was then privatized in the 1980s. In Canada, the big wave of railroad bankruptcies started after World War I, and the government nationalized a bunch of them, merged them with some existing government-founded railroads, and formed Canadian National, which was eventually privatized in 1995.

When the 1990s merger mania got going, neither Canadian Pacific nor Kansas City Southern was really in a condition to buy anything. KCS had agreed to be purchased by the Illinois Central in July 1994, but that got called off, and IC was instead purchased by Canadian National, giving CN tricoastal reach (East Coast, West Coast, Gulf Coast).

Kansas City Southern instead turned south. When Mexico was privatizing its own state-owned railroads in 1995, KCS partnered (on a 49%-51% basis) with a Mexican ocean shipping company to place the winning bid for the concession to operate Mexico’s northeastern railroads, from the Texas border (Laredo and Brownsville) down to Monterrey, Salinas, San Luis Potosi, then down to Mexico City, with spurs to the East Coast in Tampico and Veracruz and the West Coast in Lazaro Cardenas. KCS bought out their partners in 2005.

During all this, Canadian Pacific was actually selling things during 1990s merger mania. In 1997, CP sold a railroad line they had owned since the 1980s (the Iowa, Chicago and Eastern) that went from Kansas City to Chicago and thence to Milwaukee. But a decade later, they bought back that line, and it is that purchase that now allows them to potentially buy Kansas City Southern and connect their cross-Canada system to the KCS line that runs from Kansas City to Shreveport and thence down to the Gulf Coast ports and to Mexico.