Volatile Revenues For Transportation Trust Funds: A Cautionary Tale

(Ed. Note: ETW was researching efforts to provide a permanent, dedicated funding stream for federal mass transit programs in the 96th Congress (1979-1980) when we ran across an interesting set of numbers that holds lessons for the debates of the present.)

President Nixon imposed wage and price controls in 1971 as part of his efforts to fight inflation (the annual rate of which was about 6 percent at the time), and while the wage controls and most of the price controls quickly fell by the wayside, the price controls on crude oil remained in place. Combined with the global supply disruptions of the 1973 OPEC embargo, the price controls led to widespread shortages of gasoline and other petroleum products throughout the 1970s.

On April 5, 1979, President Carter addressed the nation and proposed to get rid of the price controls to ameliorate the shortages, but everyone knew that this would mean a vast increase in profits for oil companies, at least in the short term, which would be politically unpopular. Carter said that, “unless we tax the oil companies, they will reap huge and undeserved windfall profits. We must, therefore, impose a windfall profits tax on the oil companies to capture part of this money for the American people.”

In a follow-up message (H. Doc. 96-107), Carter proposed to dedicate the proceeds of the tax to a new Energy Security Trust Fund to provide aid to low-income households affected by higher energy prices, an array of energy research and conservation activities, and up to $350 million per year for mass transit.

The House passed a bill in June 1979 that would have raised an estimated $16 billion per year from the gross proceeds of the windfall tax, dedicated to an Energy Trust Fund (the spending from which was to be decided in future legislation), but House Public Works and Transportation chairman Jim Howard (D-NJ) developed an alternate use for some of the moneys. His bill (H.R. 6207, 96th Congress) would have dedicated 25 percent of the windfall profits tax receipts to a new Public Transportation Trust Fund and would have authorized $39.9 billion in additional spending for mass transit over ten years (FY 1981-1990) from the Trust Fund.

The proposed “windfall profits tax” was not actually a tax on corporate profits – that would have created even more incentives for companies to use creative accounting, writeoffs and tax shelters – but was instead an excise tax on crude oil based on the difference between the market price of a barrel and an inflation-adjusted 1979 base price. CBO Director Alice Rivlin warned Howard’s committee in July 1979 that Congress had to be careful when authorizing spending from any trust fund based on crude oil prices since the revenues “are extremely sensitive to future OPEC prices which are very difficult to project…Earmarking such an unpredictable source of revenues for programs in energy and transportation – areas where long-term investments are often needed before programs yield results – could hinder Congressional decision making.”

Congress heeded Rivlin’s advice, and the version of the oil “windfall profits” tax bill that was enacted into law in April 1980 (P.L. 96-223) did not dedicate any money to a trust fund. But what if Howard’s proposal had been successful?

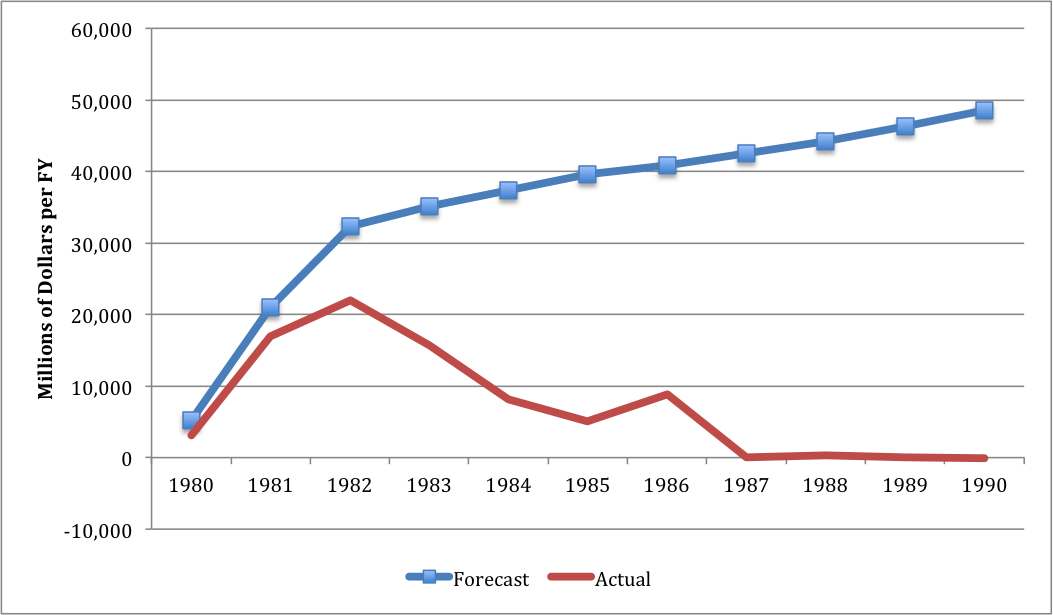

It is eye-opening to look back and see just how right Rivlin was. Here are the Joint Committee on Taxation’s revenue estimates for the oil windfall profits bill at the time the bill was enacted (the gross proceeds, 25 percent of which Howard would have earmarked for a Public Transportation Trust Fund) versus the actual revenues collected by the Treasury:

An unexpected oil glut actually pushed global crude oil prices below the inflation-adjusted 1979 benchmark by the mid-80s. If Howard had been successful in capturing 25 percent of the gross proceeds of the tax for mass transit, then in the 1987-1990 period, his trust fund would have had essentially zero dollars coming in to liquidate the outlays from over $5 billion per year of new spending commitments.

The oil windfall profits tax serves as a cautionary tale for those who would solve the Highway Trust Fund’s current revenue problems by tying future receipts to extremely volatile commodity prices (like the price of a barrel of crude oil or the price of a gallon of gasoline) or those who would fund the Trust Fund by other mechanisms that are extremely hard to predict (like how many corporate CEOs will decide to voluntary repatriate overseas corporate income to the U.S. for a one-time tax holiday).