New York City MTA Proposes Mammoth $55B 5-Year Capital Plan

The New York Metropolitan Transportation Agency this week released an outline of its proposed capital plan for fiscal years 2020-2024. The plan proposes a total of $54.5 billion in capital spending, which is $22.3 billion more than the $32.5 billion under the last iteration of its 2015-2019 capital plan.

All the information we have so far on the new plan comes from an 11-page presentation released this week. We can compare it to the detailed document of the last iteration of the previous plan we could find, the April 2018 amendment.

The MTA is unusual in that it is not really a direct subdivision of either the state or city government – it is a public benefit corporation under New York State law, which has meant that the state governor and city mayor can (and usually do) argue about who is actually in charge of the MTA and how the funding burden should be distributed. (It is like the Port Authority of New York and New Jersey in this respect – neither state can really be said to be in charge, and each state blames the other when something goes wrong.)

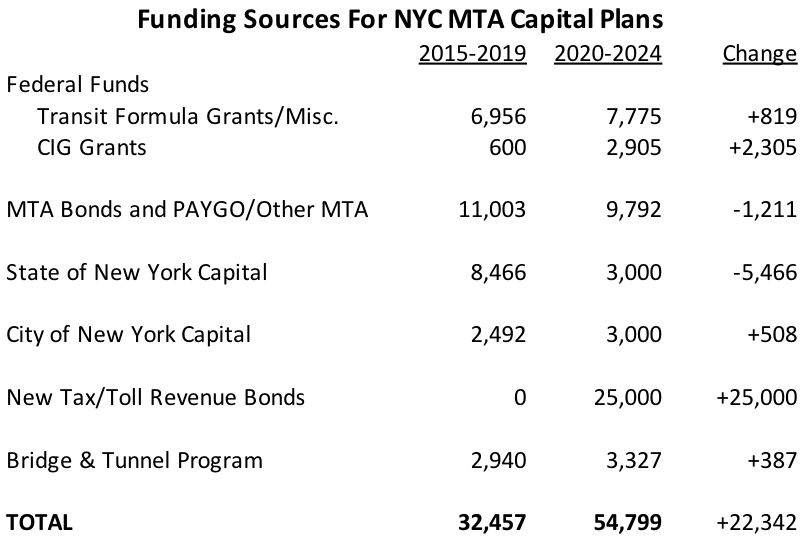

After years of stalemate and stagnation, an agreement was reached this year where the amount of direct appropriations from New York State would be reduced substantially, but the state legislature would also approve new taxes in NYC, the proceeds of which could be securitized and allow the immediate issuance of massive amounts of revenue bonds.

The overview of the proposed 5-year plan is as follows:

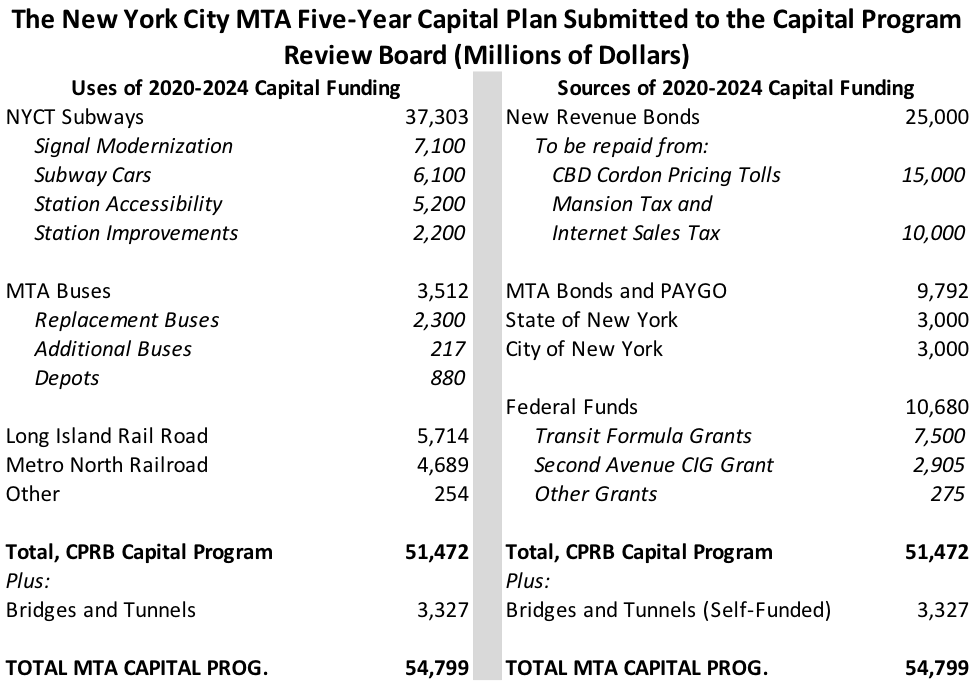

Revenues. The core of the new plan is the staggeringly large (comparatively) $25 billion in new bond issuances to be repaid from the future proceeds of congestion pricing tolls in the NYC central business district ($15 billion), the new graduated sales tax on homes over $1 million in value, and the new Internet sales tax (those latter two are supposed to collectively support $10 billion in bonds, split roughly 50-50 – the Internet sales tax is projected to raise $320 million per year and the mansion tax $365 million per year).

It should be noted that the congestion pricing scheme, while authorized by law, is still on the drawing board (we don’t know rates, exemptions, etc. yet) and won’t go into effect until 2020 at the earliest. (The Regional Plan Association had some suggestions this week as to how it might work.) And a progressive tax on the sale of high-value homes (1.0 percent on homes in the $1-2 million range, rising steadily upwards until it is 3.9 percent of the sale of a home over $25 million) seems to be an awfully volatile revenue source to use to support bond repayment.

The new plan assumes $10.7 billion in federal funding over five years. $7.5 billion is expected to come from transit formula grants (this is realistic – NYC’s transit formula apportionments for FY 2019 totaled just over $1.4 billion, times 5 would be between $7.1 billion and $7.2 billion, so with relatively conservative annual overall program growth, this is doable). However, the document indicates that the federal Capital Investment Grant (CIG) share of Phase 2 of the Second Avenue Subway will be $2.905 billion. This is concerning for two reasons:

- In the last CIG report to Congress six months ago, the Federal Transit Administration said that the anticipated CIG share of Phase 2 of Second Avenue would be $2.0 billion, not $2.9 billion (see Table 2A, here). We are still trying to track down the reason for the change. But if $2.9 billion is the new CIG draw, then that $0.9 billion increase offsets much of last month’s reduction in the proposed CIG share of the new Hudson River Tunnel (down $1.4 billion, from $6.7 billion to $5.3 billion) in terms of total CIG money going to the NYC area at any one time.

- All of the other numbers in the new financial plan appear to be in terms of the year the contract is signed or the federal funding awarded. If this means that MTA is expecting the entire $2.9 billion CIG share of Phase 2 to be appropriated by Congress over the five-year 2020-2024 period, that would be an average annual CIG draw averaging $581 million per year, which would be by far the largest ever and would almost certainly cause FTA to downgrade MTA’s application for the funding. (Again, we are still trying to get some clarity on this.)

Spending. Highlights of the proposed spending include:

- 1,900 new subway cars for the NYCT subways (1,000 on the B-Division (the old BMT and city-owned lines, now the lettered lines), and 900 on the A-Division (the old IRT lines, now the numbered lines – the two divisions use different sizes of rolling stock). Cost: $6.1 billion.

- 2,400 new buses, including about 2,200 to replace existing buses (reducing the average age of the NYCT fleet from 5.5 years to 5.1 years and of the MTA Bus Co. fleet from 10.5 years to 3.4 years) and expanding the fleet by 175 buses. 500 of the new buses will be all-electric and the fleet will be transitioning so that all post-2029 bus procurements will be all-electric. Cost: $2.5 billion.

- $7.1 billion to be spent on subway signal modernization.

- $5.2 billion to be spent increasing subway station accessibility.

- $5.7 billion for the Long Island Rail Road, including finishing (finally, praise the Lord!!) the East Side Access project by December 2022, and adding a third track on the LIRR mainline for 10 miles to substantially increase capacity.

- $4.7 billion for the Metro-North Railroad, including the long-awaited Penn Station access and the beginning of the replacement of the Grand Central Terminal trainshed and Park Avenue viaduct.

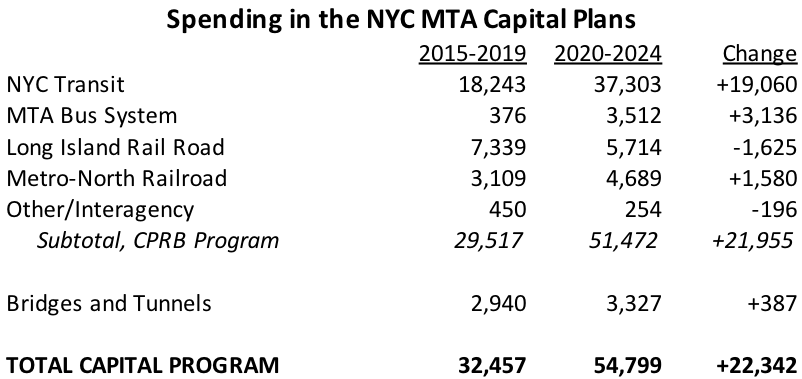

Comparison to the last capital plan. Without full documentation of the new plan, it is a challenge to compare it to the old plan. Plus, on the spending side, the old plan segregated new major capital projects into their own category and the new plan does not. When it comes to funding sources, it is obvious how the state has cut its annual appropriations burden for MTA substantially, instead providing new taxes that the MTA can use to bond:

On the spending side, we had to allocate $7 billion in capital expansion projects in the old plan to individual MTA components in order to make an apples-to-apples comparison with the new plan, and we will probably amend the following table once we get more information on the new plan.