Decline in U.S. Shipbuilding Industry: A Cautionary Tale of Foreign Subsidies Destroying U.S. Jobs

Today there is growing concern over the impact of subsidies by some foreign governments on U.S. airlines and the entire U.S. aviation system. Questions abound as to what effects subsidies by foreign governments to their national airlines have on the American aviation industry. This situation has multiple parallels with what occurred in the shipbuilding industry decades ago. An analysis of that experience provides insight into what can happen to a part of the U.S. transportation industry in the face of foreign government support of its transportation industry. This study of the American shipbuilding industry provides clues as to the potential impact of foreign subsidies on American companies, workers, and the economy.

This is a cautionary tale. The analysis shows that the effects of foreign subsidization are substantial and detrimental. Jobs that are lost do not come back. Portions of the industrial base can be eroded, thereby devastating companies, communities, and significantly impacting our national defense. Longer-run impacts can be unpredictable and have far further ramifications than originally anticipated. Put simply, a subsidized foreign industry can do significant damage to an American industry that can last for decades.

The paper is divided into three parts. The first part establishes the parallels between what happened in the shipbuilding industry in the 1970s and 1980s and what is happening in aviation today. The second part examines what happened in the shipping industry and the impact on jobs, workers, companies and communities. The paper concludes with lessons learned and applications for the current context.

Part I – Shipbuilding and Aviation: What Happened Then and Why It Is Relevant Today

What Happened to American Shipbuilding

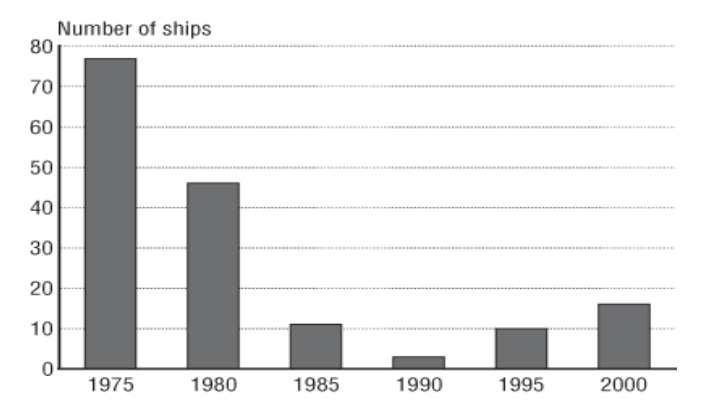

America had a long and storied commercial shipbuilding industry. After the Second World War, American shipbuilding was at its peak, leading the world. As one news story noted in 1985, “Thirty years ago, U.S. shipyards built most of the world’s fleets.”1 In 1975, America was building more than 70 commercial ships. Then the bottom dropped out of shipbuilding. Here is the decline in production of commercial shipbuilding in the United States shown graphically.2

Today, America ranks nineteenth in the world for commercial shipbuilding, accounting for approximately 0.35 percent of global new construction.3 Put another way, only one-third of one-percent of new commercial shipbuilding occurs in the United States, despite the fact that we are the world’s largest economy. What happened?

While there were many factors at play in the decline of the shipbuilding industry, including global oversupply, recessions, and changing economic fundamentals, one policy decision stands out. For many years, countries around the world subsidized their national shipbuilding industries. The U.S. did so for a time through the payment of construction differential subsidies (CDS), but ceased this practice in 1981. When foreign shipbuilding companies gained the advantage of subsidization from their governments and the U.S. shipbuilding companies had no comparable advantage, it was impossible for the American shipbuilding industry to compete. That scenario – U.S. companies competing against companies subsidized by foreign governments – is what the U.S. airlines are facing today. Here is what happened in shipbuilding to create this un-level playing field and its ramifications.

In the absence of any government action to enforce fair market participation, the U.S. commercial shipbuilding industry suffered a steady decline in the 1980s as it struggled to compete against subsidized foreign competitors. Per one U.S. Navy report, between 1987 and 1992, the industry “sold only eight commercial ships over 1,000 gross tons, compared to 77 ships annually in 1975.”4

In contrast, as one maritime analysis put it: “The Japanese, Korean, and European Governments made it a standard practice to support their shipbuilding subsidy programs.”5 As another analysis by the corporate research firm Dun & Bradstreet concluded: “Japanese and South Korean shipbuilding industries received substantial government support during the 1970s and 80s, which helped them to emerge as top players in the world. While the South Korean government significantly bolstered the industry under its Heavy and Chemical Industrialization (HCI) policy, which included capital incentives, trade incentives and tax holidays, the Japanese government provided large subsidies in the form of easy finance and loan deferments.”6 It is important to recall that Japan’s economy was booming in the 1980s. In 1981, Japan’s GDP per capita was almost three-quarters of America’s, and by 1987 it would exceed America’s.7 Similar to the situation with Gulf nations, it was developed nations engaging in strategic competition with the United States.

Given foreign government subsidization and no corrective action by the U.S government to resolve the imbalance, it was not surprising, then, that the U.S. shipbuilding industry migrated overseas. As a quote in the Los Angeles Times illustrated:

‘It’s very difficult if not impossible for U.S. shipyards to compete with foreign shipyards,’ adds Rex Sherman of the American Association of Port Authorities.”8

Foreign government subsidies of shipbuilding have continued. In 2005, the World Trade Organization (WTO) ruled that South Korean shipbuilders were benefiting from illegal export credits.9 That finding was triggered because of a complaint by the European Union, interestingly, not from the United States. The European Parliament conducted an investigation into South Korea’s shipbuilding program which concluded: “The investigation into subsidies had been granted to Korean shipyards through both export and domestic programs, which contradicted the WTO’s 1994 Subsidies Agreement.”10

The impact of these trends is clear: when the playing field ceased to be level, the bottom dropped out of the U.S. shipbuilding industry. Today, South Korea has 37 percent of global ship construction, Japan has 27 percent, and China has 21 percent.11 In other words, South Korea is producing more than 100 times the amount of ships as the United States.

What This Means for Aviation Today

The shipbuilding and aviation industries share a multitude of commonalities. Both are transportation businesses with significant economies of scale. Each industry serves a vital role in the nation’s economy with major effects across its own supply chain. Within that supply chain are important national defense considerations. Domestic ship construction supports the Navy and Merchant Marine, for example, and the domestic aviation industry works alongside the Departments of Transportation and Defense to operate the Civil Reserve Air Fleet. Most importantly, both create middle class jobs.

Just as the American shipbuilding industry confronted a situation in which foreign competition was being subsidized in the early 1980s, the American aviation industry is facing a similar situation today. Three Gulf-based airlines, Emirates, Etihad, and Qatar Airways, have received more than $42 billion in subsidies from their governments.12 These subsidies coincide with current and planned growth in operations by these airlines in the United States.13 A recent analysis of this growth in service concluded that, “Gulf carriers’ expansion to the United States has failed to meaningfully stimulate additional traffic…. Because subsidized Gulf carrier capacity additions have failed to meaningfully stimulate additional traffic to/from the United States, Gulf carrier share gains have come at the expense of U.S. and other carriers.”14

Indeed, Gulf nations are using government policy at home to help create differential costs of labor in their home countries to compete. These foreign governments are pursuing policies to keep labor costs low. One recent study found these lower labor costs “are the result of deliberate government policy decisions to suppress labor rights and thereby give artificial cost advantages to airlines based in some of the wealthiest countries in the world.”15 In other words, these governments are leveraging unfair trade practices to depress the cost structure for their own firms in aviation, just as other foreign governments did in the shipbuilding industry.

The end of a level playing field in aviation, with U.S. companies facing direct competition from subsidized foreign carriers, is remarkably similar to what happened to U.S. shipbuilders in the 1980s. If these foreign carriers are indeed successful in shifting traffic from American companies to their own, then American aviation will suffer. If the case of shipbuilding is the right analogy, the extent of that suffering, in terms of jobs lost, the impact on workers and the impact on communities, will run deep and wide.

Part II – Impact on Jobs, Workers, Companies, and Communities

Shipbuilding Jobs: The decline in the nation’s shipbuilding industry decimated a once thriving industry. In 1980 there were approximately 180,000 jobs in private shipyards.16 That number has fallen by over 40 percent, with only 105,500 jobs still existing in private sector shipbuilding according to the most recent U.S. Economic Census.17 More than four out of every ten jobs in shipbuilding that existed in 1980 are gone today.

This decline is even more striking when one considers that the nation’s labor force was much smaller in 1980. Back then, there were approximately 168 million potential workers in America. By 2010, that figure had risen to more than 233 million, according to the Bureau of Labor Statistics.18 Thus, if shipbuilding employment had simply kept constant as a percentage of the labor market, one would have expected to find more than 250,000 jobs in American shipbuilding by 2010. Instead, the nation had just over 105,000 jobs, meaning that 145,000 had been lost in the industry, taking into account population growth in the labor force.

The full economic impact of these lost shipbuilding jobs is much greater. The Department of Transportation has found that employment from shipbuilding and repair is roughly 100,000 direct and 400,000 total jobs, a ratio of approximately four to one.19 That means that every direct shipbuilding job is supported by or creates three other jobs – e.g. the engineers designing the ship, the steel workers producing what will become the ship’s hull, the accountants tracking the project, etc. Thus, the missing 145,000 jobs in shipbuilding directly translate into a loss of 580,000 jobs for the entire economy. That is a missing employment base equal to one out of every three private sector jobs in Oregon.20

The loss of American jobs as a result of subsidized foreign competition has been particularly evident in parts of the country that had been major U.S. centers for shipbuilding, such as Louisiana. In the words of then-U.S. Senator John Breaux (D-LA): “My involvement with the issue of unfair foreign shipbuilding practices relates to my State of Louisiana being one of the premiere shipbuilding States in the country. Over 27,000 Louisiana jobs are impacted by constructing or repairing ships. As has been the case nationwide, Louisiana’s ship building employment has suffered significantly since the 1980’s. This situation is due to U.S. defense downsizing and to unfair foreign shipbuilding practices….Governments in all the major shipbuilding nations, with the exception of the United States, dramatically increased aid to their shipyards and their associated infrastructure with massive levels of subsidies in virtually every form…”21

Louisiana was hardly alone in suffering from the decline in shipbuilding. The state of Maine also has a long shipbuilding history, with Bath Iron Works at the forefront. Once a major industry player in commercial shipbuilding, Bath Iron Works has not produced a single commercial ship since producing two tankers in the 1980s. To remain viable, the company has since focused solely on naval contracts. Today Bath Iron Works’ personnel stands at less than half of its employment in the 1980s.22 At more than 6,500 workers, Bath Iron Works is still the fourth largest private employer in Maine.23 This means that the jobs lost at Bath Iron Works alone are greater than the jobs currently held at any other company in Maine except three (Wal-Mart/Sam’s Club, Hannaford Brothers, and Maine Medical Center). Put another way, the jobs lost at Bath Iron Works since the end of commercial shipbuilding are greater than the entire employment within Maine of one its most famous companies, L.L. Bean.

Aviation Jobs: There are approximately 400,000 workers in the United States who work directly on scheduled passenger air transportation.24 It has been estimated that each aviation job creates 4.73 total jobs in the economy, through indirect and induced employment and economic growth. 25 That figure is roughly in line with the Department of Transportation’s estimate for shipbuilding of 4:1 mentioned earlier. Thus, scheduled passenger aviation supports about 1.9 million total jobs in the U.S. economy.

Calculating the jobs lost as a result of a specific flight ceasing to exist is slightly more complicated. For example, consider a single daily round-trip international service for a U.S. carrier using a Boeing 777, one of the planes most frequently used on the routes facing subsidized competition. Consider the simple case of that international level of service, or route, consisting of two planes flying, one each direction, every day. Each plane supports (both directly and indirectly) approximately 200 jobs – including not just the crew flying the plane, handling the baggage, and performing maintenance, but also running the entire company’s operation.26 In addition to those jobs, there are another 62 aviation jobs created as a result of the additional traffic from these flights – namely the passengers who transfer after arriving in the United States, headed to another final destination.27 We are now at 462 aviation jobs directly created by this daily service. Using simple arithmetic that translates into a total of 2,185 jobs created by this service through the entire economy using the multiplier discussed above.

Using a different framework leads to a similar finding. The Oxford Economics model took a more conservative estimate, looking only at the airline jobs created and estimated the additional job creation from just those jobs.28 While this study considered the standard indirect and induced job creation from airline employment, it did not include additional airport security or more employees at airport stores. Still, using Oxford’s more conservative job multipliers, this daily round trip international service would create more than 1,730 jobs.29

These two approaches give confidence that the loss of a single daily round-trip international service route would result in somewhere between 1,700 and 2,200 jobs being lost. It should put the importance of this debate in context that each daily round trip route of this level of service is worth approximately 2,000 American jobs.30

If the service is not eliminated but merely transferred from a U.S. carrier to a foreign carrier, not all of these American jobs would be lost. However, the vast majority would be lost as the driving factors behind both models are the jobs created behind the scenes, through the broader company, and the economic effects of employees spending their paycheck creating economic growth where they reside. An attempt to quantify the number of American jobs resulting from a foreign Gulf carrier taking this route found that only about 15 percent of the American jobs would remain in the event of a switch.31 If one takes the 2,000 jobs estimate derived above, that would mean that 1,700 American jobs would be lost as a result of a switch on a single daily route between a U.S. carrier and a Gulf carrier.

If this is the specific job loss from one daily route, it is important to consider the broader picture of aviation and the potential impact of these subsidies. The right way to consider the subsidized Gulf carriers is not only on traffic to those nations, but traffic through those nations, including travel to India and the Indian subcontinent. As one study found: “subsidized Gulf carrier expansion has also severely undermined U.S. carriers’ ability to expand their non-stop service from the United States not only to the Indian subcontinent and other growing regions of the world, but also to the hubs of their joint venture or other alliance partners in Europe or Asia, where many U.S. carrier passengers make connections to/from their overseas destination.”32 Another study reported, “Gulf carriers’ share of U.S.- Indian Subcontinent bookends more than tripled, while U.S. carriers and their joint venture partners lost nearly 800 bookings per day.”33

The Indian subcontinent currently has a population of 1.7 billion, or almost a quarter of the Earth’s population, and is expected to include another 630 million people over the next thirty-five years. Thus, it is hard to over-estimate the potential impact of that region.34 Further, about 60 percent of the world’s population lives within six flying hours of the Gulf.35 The potential for future American aviation business to be undermined by subsidized competition in additional markets is significant.

Aviation is a network industry. In a network, the impact of changes in competition, growth, and service in one region can ripple through the entire system. It is beyond the scope of this paper to produce a precise estimate of what share of the aviation industry would be likely to be affected by the foreign subsidized competition of the Gulf carriers now, and if allowed to continue, over the future. What we do know is that it will be far greater than the single round-trip scenario estimated above whose elimination would mean 2,000 American jobs lost or whose transfer to a foreign carrier would result in the loss of 1,700 jobs in the United States.

In the shipbuilding scenario, 40 percent of jobs in direct shipbuilding were lost over a more than thirty-year period. However, the number of jobs lost in shipbuilding, compared to what it would have been had shipbuilding stayed a constant share of the nation’s labor force, almost doubled. As aviation, like shipping, is fundamentally tied to the nation’s economic and population growth, it should be expected to grow on par with the nation’s overall economy. But this projected growth cannot happen if the domestic industry is unable to compete and thrive due to subsidized foreign competition.

To be clear, this is not a prediction of aviation job loss on the scale of what happened with U.S. shipbuilding. While there are many parallels between the shipbuilding and aviation industries, there are important differences. Within shipbuilding there were broader economic forces at play, and the negative effects in aviation may also be smaller given the larger proportional share of U.S. aviation that is domestic compared to shipbuilding, and hence not subject to direct competition from foreign subsidized carriers. Nevertheless, another factor driving the decline in shipbuilding was overexpansion of capacity in the 1970s – a concern also present in the airline industry today given the rapid expansion of the Gulf carriers.

However, if the impact results in only one-quarter of the impact of what happened in U.S. shipbuilding, then the U.S. could see job losses of almost 200,000 when considering direct losses in the passenger aviation business and among those jobs that are supported by passenger aviation. That figure is based on current employment and does not attempt to project for future employment, which was far greater for U.S. shipbuilding. Put another way, job losses on this level would exist if approximately 115 daily international U.S. routes were lost (transferred) to subsidized foreign competition, based on the analysis above. That might sound high today, but consider that there are already 24 daily flights into the United States from subsidized Gulf Carriers and this will grow to 30 daily flights by the end of 2015.36

Workers: Aviation and shipbuilding have another factor in common: they both create quality, middle class jobs. The average wage for an airline employee is about $67,000, almost 50 percent higher than that of the typical private sector employee.37 The average wage for a worker in shipbuilding is $73,000, which, similar to aviation, is well above the national average worker’s salary.38

Thus, the jobs that are at risk in aviation and that were lost in shipbuilding are good middle- class jobs. These are exactly the type of jobs that our economy needs to support and sustain a strong middle class. According to the Congressional Budget Office, the average middle class family’s income from work was just under $50,000 a year.39 For the average family, the fourth quintile, that is the 60th-80th percentile of wages, income from work was $83,300. Thus, jobs in aviation, which average $67,000 per worker, offer a relatively straightforward path to entry into the fourth quintile for two worker families.

Policymakers on both sides of the aisle frequently emphasize the need to expand and protect middle class jobs. House Speaker John Boehner (R-OH) defined the challenge and opportunity for the new Republican Congress as “To pass common-sense solutions that will help expand opportunities for middle-class families and small businesses.”40 President Obama’s most recent State of the Union address called for, “Practical proposals to speed up growth, strengthen the middle class, and build new ladders of opportunity into the middle class.”41

Thus, policymakers from both parties ought to be particularly concerned about and focused on issues that affect jobs in aviation, shipbuilding, and other industries where employment is particularly weighted toward middle class jobs. This is true in aviation and other transportation and infrastructure related sectors of the economy. Indeed, the U.S. Treasury Department has concluded that 90 percent of jobs created in the top three areas of infrastructure investment (construction, manufacturing, and retail trade), which account for 80 percent of total job creation, are middle class jobs.42

Communities: Aviation and shipbuilding are also industries where the employment base is more concentrated in specific communities. Unlike national chains, they are heavily localized and form the backbone of a community. For shipbuilding those communities were the ones that housed shipbuilding yards. In aviation, those communities are where ‘hub’ airports are located.

These centers – hubs and yards – are vital components of the communities in which they are located. Because both industries are capital intensive and use central locations for business, there is the potential for job loss to be non-linear. Specifically, when conditions are bad enough, a decision can be made to ‘shut the plant’ or ‘eliminate the hub’, in which, instead of simply losing a few jobs, the entire employment base in that community vanishes. This type of loss can be devastating to the community in which it is located, precisely because there are many more jobs that work with or are created by the presence of the yard or hub.

For instance, when shipyards went from producing 75 commercial ships a year in 1975 to only around five in 1985, this triggered massive yard closures. Half of the 12 major shipyards operating in America in 1980 have since closed.43 While this decline is dramatic, the effect on commercial shipbuilding is worse, as many of these remaining shipyards have focused on military shipbuilding. According to one estimate, the number of shipyards producing only commercial ships declined from 11 to only one in a year period.44

Take one example in Philadelphia, which was home to Sun Shipyards, located in Chester, Pennsylvania a community within the Philadelphia metro area. Ships were built in that yard from 1916 until it was closed in the 1980s. A study of the company found that among the factors that led to its demise was ‘increased foreign competition,’ which was listed first among other broader economic trends in the shipping industry and overall economy.45 That foreign competition was subsidized, leaving the company scrambling to stay afloat in a skewed market. In 1980, Sun Shipyards’ direct workforce stood at 4,100 employees, a slight increase from a year earlier, according to a Department of Transportation study of shipyards.46 The yard was working on several commercial ships, including container ships and tankers.47

The demise of the company meant the end to those 4,100 jobs. Using the Department of Transportation’s job multiplier, that would translate into the more than 16,000 jobs lost as a result of the closure of the plant.

One effect on the city of Chester and the broader community can be seen in the decline in population as jobs and people fled the area. The city of Chester, already in decline in 1980, had a population of just over 45,000, with the broader Philadelphia city and county having a population of over 1.68 million in 1980. The city of Chester lost 25 percent of its population between 1980 and 2010, while Philadelphia lost more than 140,000 people, or just fewer than 10 percent of its population, over that time period.48 Of course, broader economic factors were also at play, but it is logical to assume that when job loss of this magnitude takes place, workers and their families are likely to pick up and leave. The community becomes permanently changed. Today, in the shipyard’s former physical location is a state penitentiary and a casino.49

For aviation the analogy to having a shipyard is to be a hub city. That means that one or more airlines have chosen the city to locate a ‘hub’ of activity connecting the city directly to both the other hubs and spokes of that airline’s network. In addition to concentrating jobs in hub cities, hubs create direct links to other cities, facilitating easier trade and commerce. Being a hub city can have significant direct and indirect economic benefits. One study found that, “the existence of a hub airport in a region increases that region’s new economy employment by over 12,000.”50

Using the prior estimate of direct to indirect jobs supported by aviation, the creation of 12,000 jobs for the entire community as a result of being a hub would indicate direct aviation employment of just over 2,500. However, there are strong reasons to believe that the ratio of indirect jobs created would be higher in a hub city than the overall average. This is because the hub city’s other employers enjoy substantial benefit from being located near a hub city than would a community in a typical aviation environment (a ‘spoke’ as compared to a hub). In addition, businesses in that city that cater to travelers (hotels, restaurants, etc.) would likely see increased demand and hence employ additional workers. Thus, the loss of status as a ‘hub’ city in aviation would be detrimental to any city.

It is a misconception that only the nation’s largest cities serve as hubs. Major U.S. network airlines have hubs in Charlotte, Cleveland, Salt Lake City, and Minneapolis to name a few.

While these hubs may not directly serve the same markets that Gulf-subsidized carriers are serving, they are nonetheless vulnerable to potential closure due to the negative economic effects that can reverberate through the aviation network. One of the main purposes of a hub is to collect passengers from multiple smaller spoke cities and connect them to flights to larger markets that are further from or that generate less traffic than the individual spoke (hence why there is no direct flight). Critical among those larger market flights that drive this hub system are international flights, and to the extent that international flights are eliminated by U.S. airlines, hubs begin to lose some of their economic value.

That loss would have a marginal effect on the decision to keep a city as a hub. The exact tipping point varies for each hub for a variety of reasons, of which this is just one. That said, on the margin, it is conceivable that a loss of international routes could turn a hub from being profitable to unprofitable and as a result face elimination.

Potential losses affect not only hubs but also the spoke cities across the United States served by U.S. network airlines. Many of these smaller communities are not served by other U.S. carriers.51 And although these small cities are not served directly by the subsidized Gulf carriers, they are very much at risk of losing air service if U.S. carriers are forced to shrink their hubs and pare back less profitable flying due to subsidized foreign competition on international routes. Loss of service for these small communities would mean a loss of jobs and economic opportunity for some businesses in the local area.

Conclusion:

Industries change and national competitiveness within an industry can change as well. However, that change should be the result of free and fair competition, not as a result of foreign government subsidies. When American companies face foreign subsidized competition, there can be sharp and disastrous effects. This happened to American shipbuilding and it could happen to American aviation.

Those concerned about American workers and middle-class jobs should be particularly focused on aviation jobs, as they are the type of middle-class jobs that are the key to propelling sustainable and inclusive economic growth. The loss of aviation jobs will have substantial direct and indirect effects through the loss of additional jobs in businesses within the community. For every 100 jobs lost in aviation, almost 475 more are lost as a result of these direct and indirect effects. Those additional job losses are particularly acute in ‘hub’ cities, with estimates as high as 12,000 jobs riding on just being a hub.

Fortunately, there is still time to act and Congress has already shown signs of responding to this current situation. In April 2015, a majority of members of the U.S. House of Representatives signed a letter to the Secretaries of State and Transportation urging them to get involved “in an effort to stem the tide of subsidized capacity that state-owned airlines are deploying on international routes to the United States.”52 Those members of Congress appreciated the potential ramifications to the broader economy when they wrote, “Failure to address these practices [foreign subsidies] will lead to significant job losses in the United States and set a dangerous precedent that could lead to further harm to the U.S. airline industry and the broader U.S. economy.”53

Whether congressional or executive branch intervention is able to adequately address the situation remains to be seen. However, if the current case of American aviation being forced to compete with subsidized foreign carriers follows the path of what happened in the shipbuilding industry, the prediction of the majority of members of the U.S. House may become true at a level that would exceed anyone’s expectations.

About the Author:

Aaron Klein served at the U.S. Treasury Department as Deputy Assistant Secretary for Economic Policy, Policy Coordination. He led the Treasury Department’s work on infrastructure policy, representing Treasury both internationally and within the executive branch. Klein also worked extensively on financial regulatory reform issues including crafting and helping secure passage of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010. Prior to his appointment in 2009, he served for over eight years on the staff of the Senate Banking, Housing and Urban Affairs Committee, including as chief economist. He is a graduate of Dartmouth College and the Woodrow Wilson School for Public Affairs at Princeton University.

1 Associated Press, Shipyard Closing Reflects Decline of a U.S. Industry, Los Angeles Times, August 8, 1985

2 U.S. Department of Transportation, Transportation Statistics Annual Report 2001, Figure 1: https://www.rita.dot.gov/bts/sites/rita.dot.gov.bts/files/publications/transportation_statistics_annu al_report/2001/html/chapter_05_figure_01_132.html

3 U.S. Department of Transportation, Maritime Trade and Transportation, 2007, Table 7-2 https://www.rita.dot.gov/bts/sites/rita.dot.gov.bts/files/publications/maritime_trade_and_transport ation/2007/html/table_07_02.html

4 Shipbuilding, available at Homeland Security Digital Library: https://www.hsdl.org/?view&did=1759, page 15-3

5 The Future of American Shipbuilding, Marinelink.com, https://www.marinelink.com/article/shipbuilding/the-future-american-shipbuilding-805

6 Dun and Bradstreet, Shipbuilding: Regulatory and Policy Benchmarking, https://www.dsir.gov.in/reports/isr1/Shipping/9_7.pdf

7 The World Bank GDP per capita data available at: https://data.worldbank.org/indicator/NY.GDP.PCAP.CD?page=5

8 Associated Press, Shipyard Closing Reflects Decline of a U.S. Industry, Los Angeles Times, August 8, 1985 https://articles.latimes.com/1985-08-08/business/fi-3538_1_american-shipyard

9 Giles, Warren, WTO Finds South Korean Shipbuilding Subsidies Illegal, Bloomberg, March 7, 2005 https://www.bloomberg.com/apps/news?pid=newsarchive&sid=aWE0lGT7qzS0

10 European Parliament Fact Sheets, Shipbuilding, 4.7.3, available at: https://www.europarl.europa.eu/facts_2004/4_7_3_en.htm

11 Department of Transportation, Maritime Trade and Transportation, 2007, Table 7-2 https://www.rita.dot.gov/bts/sites/rita.dot.gov.bts/files/publications/maritime_trade_and_transport ation/2007/html/table_07_02.html

12 Britton, Rob, The Tilted Playing Field in International Airline Competition, Huffington Post, April 8, 2015 https://www.huffingtonpost.com/rob-britton/the-tilted-playing-field-_b_7028344.html

13 Emirates to make Orlando its 10th U.S. destination”, USA Today, March 24, 2015; “Emirates Adds 2nd daily Seattle Service from July”, https://airlineroute.net/2015/03/24/ek-sea-jul15/; “Emirates Adding Second Daily Dubai-Boston Flight”, TravelPulse, April 13, 2015. “Qatar Airways Set to Expand its USA Network with the Addition of Three New Routes”, Qatar Airways Press Release, May 4, 2015. https://www.qatarairways.com/global/en/press-release.page?pr_id=pressrelease_usa.

14 Lee, Darin and Amel, Eric, Assessing the Impact of Subsidized Gulf Carrier Expansion on U.S.- International Passenger Traffic, May, 2015 https://www.openandfairskies.com/wp- content/uploads/2015/05/CL-paper-on-Gulf-Carrier-Traffic-1.pdf, pages 2-3

15 ibid

16 An Assessment of Maritime Trade and Technology, Washington, D.C.: U.S. Congress, Office of Technology Assessment, OTA-O-220, October 1983, Chapter 4, page 100, can be found at: https://www.princeton.edu/~ota/disk3/1983/8302/830206.PDF

17 United States Census Bureau, U.S Economic Census 2012, NAICS code 336611 Shipbuilding and repairing. Note that this number is consistent with DoT’s analysis which estimated 107,000 jobs in ship building, The Economic Importance of the U.S. Shipbuilding and Repairing Industry, MARAD, May 30, 2013, available at: //www.marad.dot.gov/wp- content/uploads/pdf/MARAD_Econ_Study_Final_Report_2013.pdf

18 Toossi, Mitra, Labor Force Change, 1950-2050, Monthly Labor Review, May 2002, Bureau of Labor Statistics, available at: https://www.bls.gov/opub/mlr/2002/05/art2full.pdf

19 The Economic Importance of the U.S. Shipbuilding and Repairing Industry, MARAD, May 30, 2013, available at ://www.marad.dot.gov/wp- content/uploads/pdf/MARAD_Econ_Study_Final_Report_2013.pdf (page E-2)

20 Bureau of Labor Statistics, Establishment Data for State Employment, Seasonally Adjusted, Table D-1 available at: https://www.bls.gov/web/laus/tabled1.pdf

21 Congressional Record, U.S. Senate, October 23, 1995 page 28996 which can be found at: https://books.google.com/books?id=HH9KOKGZJJYC&pg=PA28996&lpg=PA28996&dq=how+many+ shipbuilding+jobs+1980&source=bl&ots=Vk5a2XHg1Z&sig=Epr5bJiFlJbJ4cXhpsPyZ7- 53kU&hl=en&sa=X&ei=88dgVdvTCIiryAS8lIGwBQ&ved=0CFEQ6AEwBw#v=onepage&q=how%20m any%20shipbuilding%20jobs%201980&f=false

22 Senville, Wayne, Keeping the Economy Afloat, PlannersWeb, Nov. 2012, available at: https://plannersweb.com/2012/11/keeping-economy-afloat/

23 State of Maine, Department of Labor, Top 50 Private Employers in Maine, 2015, available at: https://www.maine.gov/labor/cwri/publications/pdf/MaineTop50Employers.pdf

24 United States Census Bureau, U.S Economic Census 2012, NAICS code 336611 https://factfinder.census.gov/faces/tableservices/jsf/pages/productview.xhtml?pid=ECN_2012_US_0 0A1&prodType=table. This is a conservative estimate given that there are other forms of aviation that might be affected

25 Americans 4 Aviation, Creating Jobs, 2015 available at: https://airlines.org/industry/#economic

26 Partnership for Open and Fair Skies, Restoring Open Skies: The Need to Address Subsidized Competition from State-Owned Airlines in Qatar and the UAE, January 28, 2015, available at: https://www.openandfairskies.com/wp-content/themes/custom/media/White.Paper.pdf, page 51. 27 Comments on Gulf Carrier Subsidy Claims, United States Government Questions and Answers, US Docket DOS-2015-0016-001, Technical and Clarification Questions on the Gulf Subsidies Report, available at: https://www.regulations.gov/#!documentDetail;D=DOS-2015-0016-1300

28 Oxford Economics, Economic Benefits from Air Transport in the US, 2011, available at: https://www.iata.org/policy/Documents/Benefits-of-Aviation-US-2011.pdf

29 462 jobs calculated using the indirect multiplier of 1.64 and the induced multiplier of 0.42 from Oxford Economics above.

30 This analysis uses the standard point estimates for multipliers and jobs created. Given the inherent statistical variance around these estimates, I prefer to use more rounded figures, which are statistically identical to those derived from point estimates. Put another way, the exact figures multiply out to 1,731.95 jobs using the Oxford analysis. Statistically that is identical to 1,730.

31 Partnership for Open and Fair Skies, Restoring Open Skies: The Need to Address Subsidized Competition from State-Owned Airlines in Qatar and the UAE, January 28, 2015, page 51

32 Lee, Darin and Amel, Eric, Assessing the Impact of Subsidized Gulf Carrier Expansion on U.S.- International Passenger Traffic, May, 2015, page 3

33 Partnership for Open and Fair Skies, Restoring Open Skies: The Need to Address Subsidized Competition from State-Owned Airlines in Qatar and the UAE, January 28, 2015, page 47

34 Readling, Brigid, World Population Hitting 7 Billion, October 2011, available at: https://www.earth- policy.org/indicators/C40/population_2011

35 Britton, Rob, Big Three: U.S. Airlines Versus Persian Gulf Carriers, Forbes, May 2015, available at: https://www.forbes.com/sites/realspin/2015/05/12/the-big-three-u-s-airlines-versus-persian-gulf- carriers/

36 Partnership for Open and Fair Skies, Restoring Open Skies: The Need to Address Subsidized Competition from State-Owned Airlines in Qatar and the UAE, January 28, 2015, page 5

37 Americans 4 Aviation, Creating Jobs, 2015 available at: https://airlines.org/industry/#economic

38 Department of Transportation, MARAD Report: Nation’s Shipyards Support $36 billion in GDP, July, 2013, available at: https://www.dot.gov/briefing-room/marad-report-nation%E2%80%99s- shipyards-support-36-billion-gross-domestic-product

39 Congressional Budget Office, The Distribution of Household Income and Federal Taxes 2011, November, 2014 available at https://www.cbo.gov/publication/49440

40 Boehner, John, Boehner Discusses GOP Solutions for Middle-Class Families, January 2015, available at: https://www.speaker.gov/video/boehner-discusses-gop-solutions-middle-class-families

41 Obama, Barack, State of the Union Address, January 2014, available at: https://www.whitehouse.gov/the-press-office/2014/01/28/president-barack-obamas-state-union- address

42 U.S. Treasury Department and Council of Economic Advisors, An Economic Analysis of Infrastructure Investment, 2010, available at: https://www.treasury.gov/resource-center/economic policy/Documents/infrastructure_investment_report.pdf

43 White, Ronald, Full Steam Ahead for Nascco Shipyard in San Diego, Los Angeles Times, July, 2011, available at: https://articles.latimes.com/2011/jul/03/business/la-fi-made-in-california-shipyard- 20110703

44 U.S. Congressional Record, Statement of Senator Breaux, October 23, 1995.

45 Costello, John and Kavanagh, David, Sun Shipbuilding and Dry Dock Co. A Short History, Sun Ship Historical Society, 2007, available at: https://www.sunship.org/sshs_short_history001.pdf

46 U.S. Department of Commerce, Maritime Administration, Report on Survey of U.S. Shipbuilding and Repair Facilities, 1980, available at: https://www.marad.dot.gov//srv/htdocs/wp-content/uploads/pdf/1980_- _Report_on_Survey_of_US_Shipbuilding_and_Repair_Facilities.pdf

47 ibid

48 U.S. Census Department data as reported at https://en.wikipedia.org/wiki/Chester,_Pennsylvania and https://en.wikipedia.org/wiki/Demographics_of_Philadelphia

49 Dorwart, Jeffery, Shipbuilding and Shipyards, The Encyclopedia of Greater Philadelphia, Rutgers University, 2013, available at: https://philadelphiaencyclopedia.org/archive/shipbuilding-and- shipyards/

50 Button, Kenneth and Stough, Roger, Air Transport Networks: Theory and Policy Implications, Edward Elgar Publishing, 2000 page 254

51 Partnership for Open and Fair Skies, Restoring Open Skies: The Need to Address Subsidized Competition from State-Owned Airlines in Qatar and the UAE, January 28, 2015

52 Lipinski, Dan, Dold, Bob, and more, letter to Secretary Kerry and Secretary Foxx, April 30, 2015, available at: https://lipinski.house.gov/uploads/Bipartisan%20Letter%20to%20Secretary%20of%20State%20Jo hn%20Kerry%20and%20Transportation%20Secretary%20Anthony%20Foxx.pdf

53 ibid